Cite commentary

IEA (2023), How can sustainable debt support China’s energy transition?, IEA, Paris /commentaries/how-can-sustainable-debt-support-chinas-energy-transition, Licence: CC BY 4.0

Sustainable debt issuances are picking up as the global energy transition gains momentum

Sustainable debt has become a popular tool to fund green and sustainability-linked activities since it first emerged in the mid-2010s, providing a tailwind to clean energy investment. Global sustainable debt issuances have risen nearly tenfold since 2016, peaking at over USD 1.7 trillion in 2021. These instruments have been leveraged by governments to raise capital for green infrastructure, by financial institutions to facilitate green or sustainable lending, and by corporates to raise funds for their net-zero efforts. One driver of issuance has been the willingness of many investors to accept lower interest rates if a bond is classified as green or sustainable, a distinction often referred to as the “greenium.”

Sustainable debt issuances can take several forms. Green, social, sustainability and transition bonds are all considered “use of proceeds” bonds, whereby the funds raised are allocated to pre-defined activities or projects, often outlined in a guidance document known as a taxonomy. They also generally come with strict reporting and verification requirements. Green bonds are most common, accounting for nearly 40% of total sustainable debt issuances.

More recently, sustainability-linked bonds (SLBs) have emerged as a more flexible means to access the green debt market. SLBs have a unique structure whereby the interest paid to bondholders can vary based on the issuer’s achievement of certain sustainability targets, such as reducing emissions intensity or absolute emissions. Unlike use of proceeds bonds, they are not tied to specific activities or projects. This flexibility means they have been favoured by carbon-intensive industries that need to finance transition activities more broadly, as well as by sovereign issuers, since public finance management practices, sometimes enshrined in law, may preclude the use of funds for a specific purpose.

Sustainable debt issuances by theme, 2014-2022

OpenGrowth in the sustainable debt market is particularly remarkable in China

The People’s Republic of China (hereafter China) has emerged as one of the fastest growing adopters of sustainable debt instruments. Most of the growth to date in the Chinese market has been driven by green instruments, which accounted for just under 70% of sustainable debt issuance in 2022. The vast majority of these issuances are bonds, which reached RMB 875 billion (USD 120 billion) last year. This makes China the world’s second largest market for green bonds behind the United States, a position it has held since 2021. And there is still substantial room for further growth. Labelled green bonds, for example, only account for only around 1.5% of the country’s total onshore bond market.1 By contrast, green loans, which reached around RMB 22 trillion (USD 3 trillion) in 2022, already constitute around 10% of the country’s total loan market.

Sustainable debt issuance by type in China, 2016-2022

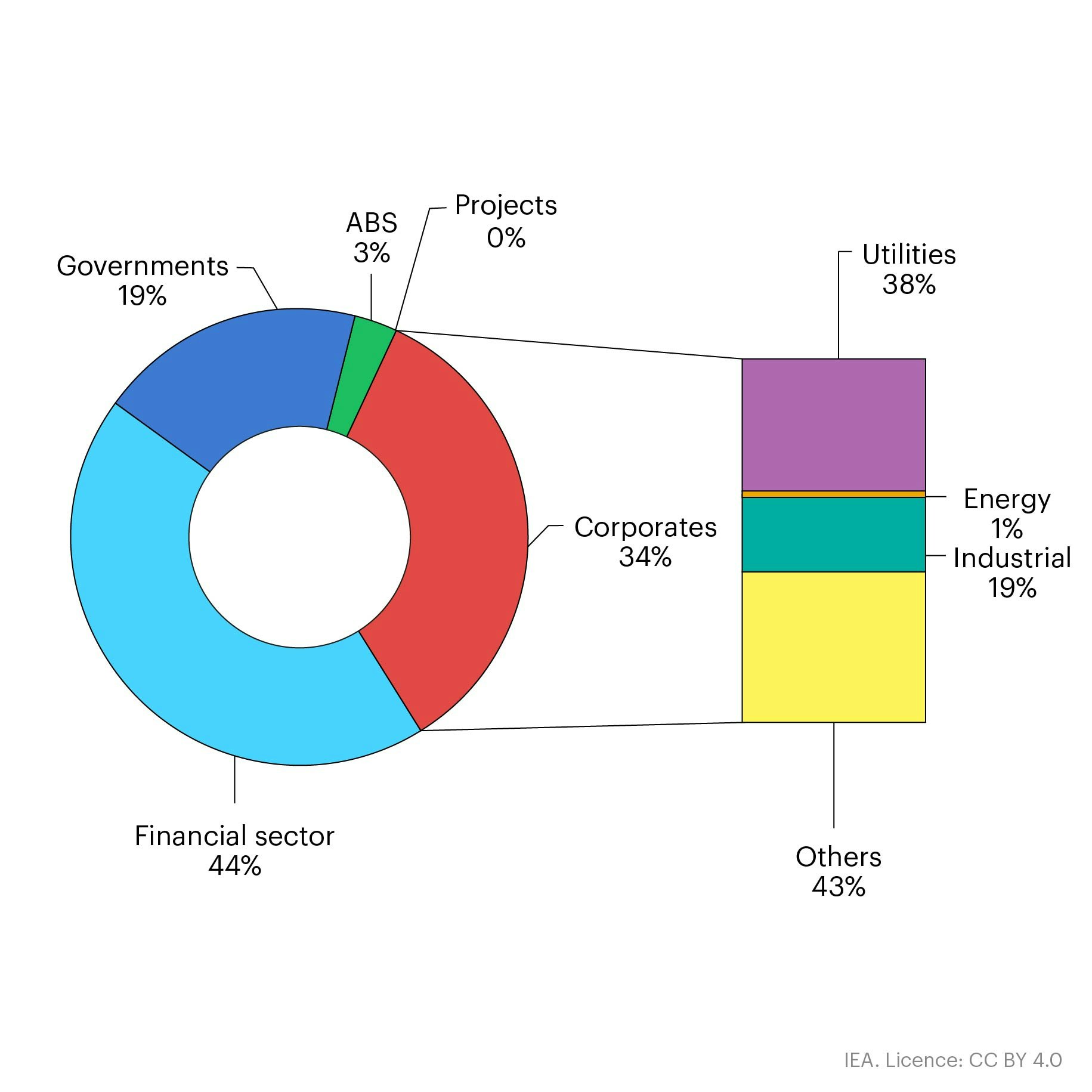

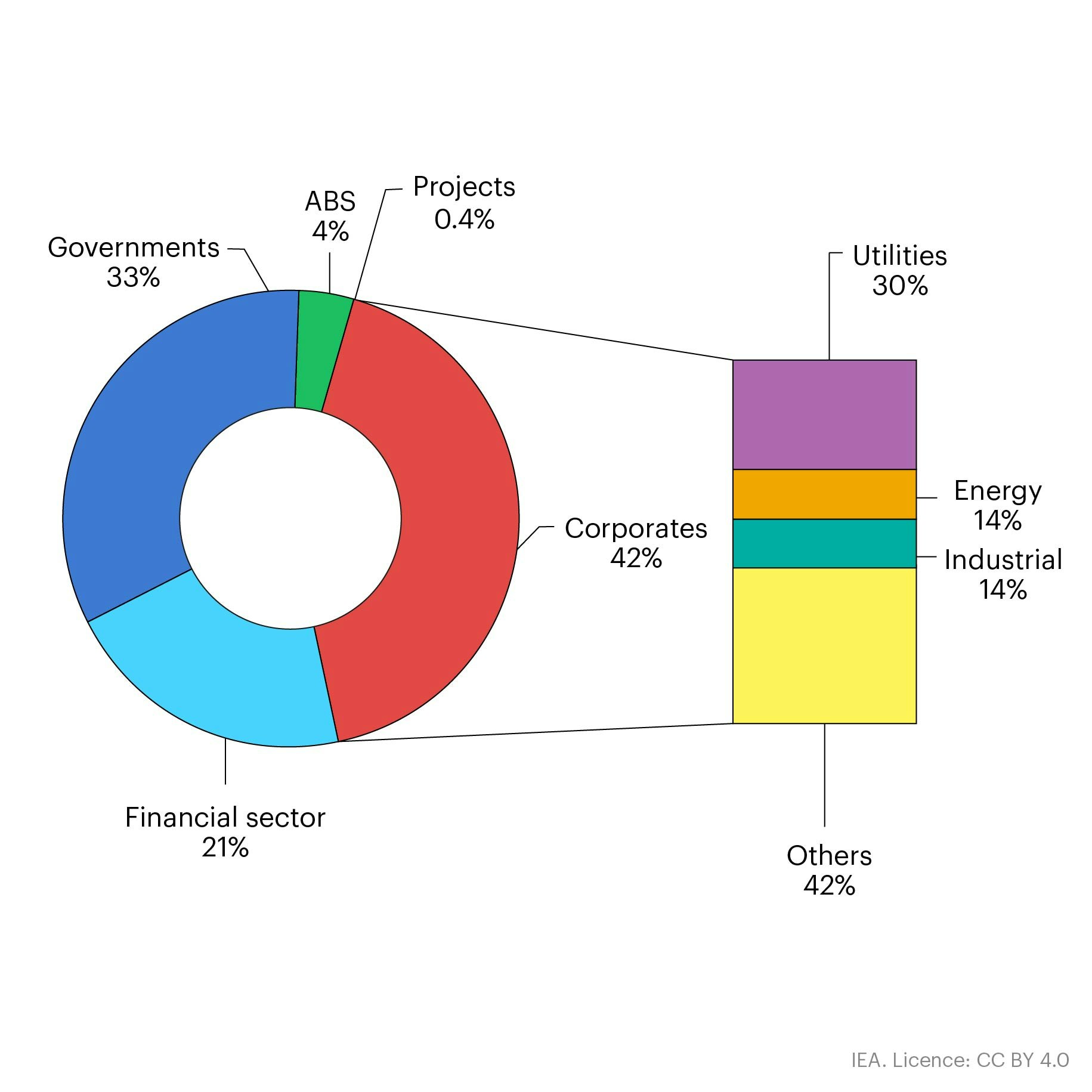

OpenThe drivers of growth in China’s sustainable debt market, as well as the beneficiaries, look different than in OECD economies, where sustainable finance tends to be the domain of the private sector. In China, meanwhile, state-owned banks have facilitated much of the rapid expansion in the market, providing indirect financing for prominent firms across the energy, power and industrial sectors, many of which are state-owned. Banks in China account for 45% of activity across all sustainable debt categories, compared with only 20% in OECD economies.

Another notable difference is that in China’s onshore market, the “greenium” is largely absent, according to analysis from early 2023. This is likely the result of an oversupply of green opportunities. While policy banks and state-owned enterprises have driven the rapid rise in issuance to meet China’s carbon neutrality targets, this has not been met with rising interest for buyers, reducing pricing benefits.

Characteristics of sustainable debt issuances in China, 2016-2022

Open

{kind=link}

Characteristics of sustainable debt issuances in advanced economies, 2016-2022

Open

{kind=link}

The Chinese market demonstrates the impact of policy to drive sustainable finance

There are broader lessons to take from the swift growth in China’s sustainable debt market, even with its unique characteristics. The lack of a “greenium,” for example, means robust government policy has played a major role in the market’s development – an important takeaway for other markets in which this trend emerges.

The Chinese government supported the launch of the domestic green bond market when the People’s Bank of China (PBOC) and six other government agencies issued the Guidelines for Establishing the Green Financial System in 2016. Since then, the development of the market for green, sustainable and transition finance instruments has been driven by strong policy support.

However, there are still challenges to overcome in the regulatory environment. Four regulators oversee the sustainable debt market in China: the PBOC, the China Securities Regulatory Commission (CSRC), the National Association of Financial Market Institutional Investors (NAFMII) and the National Development and Reform Commission (NDRC). An inter-governmental authority published the Green Bond Principles in July 2022 with the aim of harmonising these regulations, but the NDRC – which is responsible for bonds by state-owned enterprises – has not yet adopted them. Under the Principles, a bond can only be labelled as “green” if 100% of the capital raised is allocated for green activities, whereas the NDRC has a threshold of only 50%. Bonds by state-owned enterprises accounted for about half of onshore green issuances between 2019 and 2022, indicating the scale of this potential regulatory gap.

Policies and regulations relating to sustainable and green finance in China

|

Policy name |

Date |

Details |

|---|---|---|

| Green Credit Guidelines | 2012 | Issued by the China Banking Regulatory Commission. The regulator encouraged banks to consider environmental and social risks within their lending practices, as well as to publish green lending strategies. |

| 2016 | Issued by the PBOC along with six other government agencies, including the CSRC. The guidelines introduced incentives such as re-lending programmes from the PBOC, green guarantees and interest subsidies. The guidelines highlighted the importance of green bonds and called for greater unity in standards across regulators. | |

| The Green Bond Endorsed Project Catalogue (2021 Edition) | 2021 | The Catalogue published by the PBOC serves as the country’s green taxonomy. It covers activities in six key areas, including energy conservation and clean energy. The 2021 edition removed “clean coal” and fossil-powered generation, including gas and LNG, from the list of green activities. |

| Common Ground Taxonomy – Climate Change Mitigation (CGT) | November 2021; updated June 2022 | Joint initiative by the PBOC and the European Commission with a list of green and sustainable activities recognised by both China and the EU. The CGT is non-legally binding. In July 2023, the PBOC announced that 193 bonds that raised 251.3 billion yuan (USD 35 billion) between 2016 and 2023 were CGT-compliant. |

| China Green Bond Principles | July 2022 | Published by the China Green Bond Standards Committee to harmonise definitions between the domestic and international green bond markets. These guidelines now require 100% of proceeds to fund green projects, instead of 50-70% as was previously stipulated. These principles do not apply to bonds by state-owned enterprises. |

| Green Finance Guidelines | 2022 | Issued by China Banking Regulatory Commission, applying to banks’ overseas lending. Under the guidelines, banks and insurers are required to terminate funding for projects with high environmental risks that do not meet international standards. |

| Transition Finance Taxonomy | Upcoming |

The PBOC announced in 2022 that it was developing a transition finance taxonomy that is expected to be in line with the G20 Transition Finance Framework. |

Transition activities also require the creation of targeted instruments, such as those emerging in China

Funding needs for China’s ambitious climate targets are high. China currently accounts for roughly 30% of global carbon dioxide emissions, and coal-based electricity accounts for over 50% of the country’s power generation. The government’s policy to reach peak CO2 emissions before 2030 is estimated to require up to USD 3.5 trillion, while carbon neutrality by 2060 could call for USD 27 trillion. The bulk of this spending is for the energy, industry and transport sectors, which the IEA estimates will require USD 18 trillion in investment between 2030 and 2050.

Special attention is necessary for the high-emitting sectors that account for 40% of China’s GDP. Electricity produces 48% of the country’s emissions, while heavy industry generates 36%. Replacement technologies in heavy industry alone could help China avoid emissions equivalent to almost 15% of the world’s remaining carbon budget, compatible with a 50% chance of keeping global warming to 1.5 °C.

Financing transition activities for hard-to-abate sectors presents a particularly unique challenge, since many do not qualify for green activities under sustainable finance frameworks. This requires a different set of taxonomies and tools, as well as credible transitions plans from enterprises. China – which was joint chair of the G20 Sustainable Finance Working Group and led the creation of the G20 Transition Finance Framework – has emerged as a key leader in this area.

The Chinese government has explored the use of transition bonds and SLBs, with the latter proving more popular due to their versatility. As at the end of 2022, SLBs and transition bonds listed onshore and offshore reached cumulative volumes of USD 16.9 billion (116 billion yuan), 74% of which were SLBs.

Despite this progress, there is still a need to address some critiques about greenwashing risks, which include concerns that issuers will not link these instruments to sufficiently ambitious climate targets. Currently, there is no national sustainable finance taxonomy in China, though the country’s central bank is due to put forward sector-specific transition finance standards – starting with steel, thermal power, construction materials and agriculture – which will go some way to addressing this.

And some localised examples are already in place. For example, Huzhou City in China’s Zhejiang province is one of the country’s green finance pilot zones, established by a 2017 initiative from the PBOC and six ministries aimed at creating tailored financial solutions to the area’s economic and social needs. In January 2022, the Huzhou City Transition Finance Catalogue was published, laying out 30 transitional activities (including technical pathways) in nine sectors. These technical pathways include indicators and performance benchmarks to support SLB issuance and avoid greenwashing.

China’s approach to transition and green finance demonstrates the crucial role of policy, particularly the value of targeting transition finance as a separate issue. In economies where state-owned entities play a dominant role, or where government-affiliated financial institutions make up a large part of the financial ecosystem, government guidance can act as the primary driver of the market if a “greenium” doesn’t materialise.

Recent developments in China also show the benefits of targeting key industries to build up familiarity with transition finance instruments. An important issue in transition finance is ensuring projects are supporting the shift to a lower-carbon future without locking in unnecessary emissions or greenwashing. Clear, science-based transition pathways are an essential part of this toolkit – as is the enforcement of taxonomies, monitoring and verification procedures. Equally important is regulatory clarity, with a risk that overlapping frameworks deter investors.

References

The Chinese bond market is divided into three categories: onshore, the largest, followed by hard currency and offshore local currency. The onshore market, totalling around RMB 140 trillion (USD 20 trillion) at the end of 2022, is the primary domain of local governments, policy banks and local corporate issuers. Meanwhile, the offshore hard currency market, totalling around USD 740 billion in early 2023, is most frequently accessed by international investors. The smallest market – offshore local currency – is primarily the reserve of sovereign issuances. Sustainable debt instruments are present across all three bond markets.

Reference 1

The Chinese bond market is divided into three categories: onshore, the largest, followed by hard currency and offshore local currency. The onshore market, totalling around RMB 140 trillion (USD 20 trillion) at the end of 2022, is the primary domain of local governments, policy banks and local corporate issuers. Meanwhile, the offshore hard currency market, totalling around USD 740 billion in early 2023, is most frequently accessed by international investors. The smallest market – offshore local currency – is primarily the reserve of sovereign issuances. Sustainable debt instruments are present across all three bond markets.

How can sustainable debt support China’s energy transition?