Cite commentary

IEA (2023), Reaching net zero emissions demands faster innovation, but we’ve already come a long way, IEA, Paris /commentaries/reaching-net-zero-emissions-demands-faster-innovation-but-weve-already-come-a-long-way, Licence: CC BY 4.0

Meeting climate targets will not require fundamentally new technology concepts, but it will require innovation

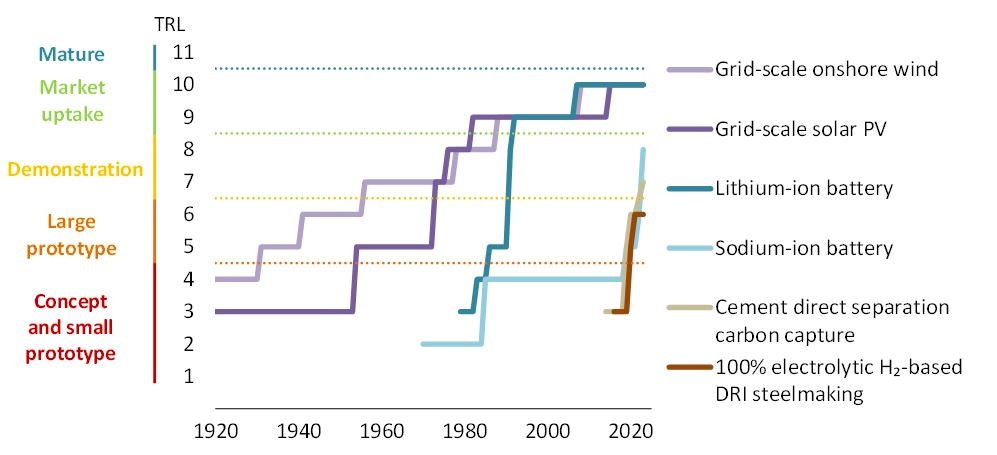

A new energy economy is emerging fast, building on a long history of technological progress. And if history is any guide, clean energy innovation can be a slow journey. For example, while the photovoltaic effect was discovered in the late 1830s and the first solar PV cell prototyped in the 1880s, technology progress only accelerated much later, in the 1950s. Solar power reached 1% of global electricity generation in 2015 only. Similarly, the first wind turbine was built in the 1880s, but wind power only reached 1% of national power generation in Denmark a century later, and 1% of global power generation later still, in 2008. The battery effect was demonstrated in 1800, but today’s well-known lithium-ion batteries were prototyped for the first time in the 1980s and reached the mass market by 2010.

Reaching net zero CO2 emissions from the energy sector by 2050 does not necessarily require fundamentally new scientific concepts or breakthroughs comparable to the initial discovery of solar, wind or batteries. However, innovation still plays an important role: about 35% of the CO2 emission reductions needed in the recently updated Net Zero Emissions by 2050 Scenario (NZE Scenario) in 2050 come from technologies that are still in development and thus have not reached markets at commercial scale. Continued innovation will also be needed to improve performance and reduce costs of technologies already delivering emissions reductions, as well as to improve manufacturing processes. But our analysis suggests that even the most ambitious technology improvements in the NZE Scenario could be considered incremental in comparison to major discoveries.

In many cases, the challenge is to bring new technologies to commercial scale in time to ensure an affordable energy transition. This calls for better designs or new combinations of existing technologies that can help to reduce costs, improve performance, address new use cases, minimise the use of critical resources, and mitigate other environmental impacts. Of course, completely new ideas may still arise, leading to new technology concepts or materials that could further accelerate the clean energy transition and broaden its scope. So even if it is reassuring that existing clean technologies can enable a net zero world, governments should continue to nurture and support early R&D to increase the chances of such breakthroughs.

Clean energy innovation is advancing rapidly

Considerable progress has been made in recent years to address pressing innovation gaps, resulting in important technology readiness upgrades. This has been reflected in the recently updated NZE Scenario: in our 2021 roadmap, the share of CO2 emission reductions in 2050 from technologies that were not yet on the market at the time of writing stood at almost half (46%), a larger share than in our 2023 roadmap.

Recent major technology developments can be consulted in the ETP Clean Energy Technology Guide, an annually updated interactive database that tracks information on more than 550 individual designs and components that can contribute to getting on a path to the NZE Scenario. It includes indicators of technology readiness and background information on R&D and demonstration projects for such technologies around the world.

Comparison of CO2 emissions reductions in 2050 relative to base year by technology maturity in the 2021 and 2023 NZE Scenarios

OpenRecent examples include:

- Road transport: In 2022, electric cars accounted for nearly 15% of total car sales, little more than a decade after they were first commercialised. This was achieved thanks to strong policy support and technology progress, such as performance improvements and cost reductions in lithium-ion batteries, battery and vehicle integration, and charging. Innovation has now turned to new challenges, such as mitigating demand for critical minerals and increasing energy density for heavy-duty applications. After 40 years of incremental progress in R&D since the first prototypes in the 1980s, innovation in sodium-ion batteries – which do not contain any critical minerals – accelerated in the late 2010s, and the first sodium-ion powered electric cars are reaching the market this year, with new supply chains being quickly established.

- Power: Construction of the first commercial small modular nuclear reactors has started, with operations expected by 2026. Floating offshore wind farms are getting larger than ever and could exceed the 1 GW mark in 2026. The first solar PV modules equipped with perovskite cells at an efficiency nearing 30% are reaching markets.

- Heavy industry: In 2021, fossil-free steel was produced for the first time using 100% electrolytic hydrogen, with plans to demonstrate industrial scale production. In 2023, final investment decisions were made to bring carbon capture demonstrators to commercial scale in cement production. And first-of-a-kind commercial production of carbon-free aluminium is expected by 2026, after the technology was first demonstrated in 2021.

- Long-distance transport: Short-haul all-electric planes for up to 20 passengers are under development and could reach commercial use by 2026. Production of hydrogen-based synthetic aviation fuels is taking place on a larger scale, and the first industrial plant to convert biogas into low-emissions bio-liquefied natural gas to replace heavy fuel oil in shipping could begin operations in early 2024.

Despite encouraging progress, innovation success should not be taken for granted. There is also a long list of innovation setbacks from the past decades, with technologies stuck in the pipeline, delays and failures. For example: solid-state battery prototypes have been experiencing delays in production; fuel-cell electric vehicles have not achieved the market potential once foreseen by large industry players; and fossil fuel-based electricity generation from facilities equipped with carbon capture – an area with several technologies currently at demonstration stage – is moving more slowly than projected just a few years ago.

Historical evolution of the Technology Readiness Level for selected clean energy technologies

Open

{kind=link}

Growing demand for clean energy technologies could further shorten critical steps in the innovation journey

Every innovation journey is different, steered by diverse government policies, advances in complementary technologies or even unforeseen events, but in many cases, innovation remains slow and risky until demand for the technology strengthens. R&D and demonstration are typically expensive, and when cheaper alternatives can already be found on the market, there are fewer incentives to innovate. In contrast, pressing needs or promising business opportunities can induce much quicker innovation. For example, increasing demand from the US aerospace industry stimulated solar PV innovation. The oil crisis in the 1970s sparked energy security concerns globally, and in countries like Denmark, strong interest in alternative sources of energy enabled faster wind technology development. The rapid emergence of microelectronics since the 1990s and electromobility since the 2010s have supported the lithium-ion battery industry.

By supporting demand for clean energy, decision makers can help accelerate innovation. The drivers of innovation in any sector are multiple and complex, but there is strong evidence that policy plays an important role. Well-designed policy support, co-ordinated among innovation stakeholders, can facilitate the building of large prototypes, carrying out capital-intensive demonstration projects, and scaling up new products. Down the road, this can help shorten each individual step in the innovation journey and compress them together.

Spending on clean energy R&D hit a record high last year, despite the global energy crisis, geopolitical volatility and macroeconomic uncertainty. Public spending on energy R&D rose to nearly USD 44 billion globally in 2022, over 80% of which was allocated to clean energy. To bring clean energy demonstration projects in line with the needs in the NZE Scenario, in 2022 16 governments committed USD 94 billion in public funding for large-scale demonstration projects by 2026. The IEA is monitoring clean energy demonstration projects to improve global understanding of technology coverage, total public funds spent and private co-investment unlocked as a result. Major policy developments of the past few years, such as the Inflation Reduction Act in the United States, the Net Zero Industry Act in the European Union, and China’s latest Five-Year Plan, will also have an impact on clean energy innovation and technology development.

On the corporate side, energy R&D spending by globally listed companies exceeded USD 130 billion in 2022, up 10% year-on-year and returning to the pre-Covid trajectory. Spending by companies developing renewables increased by 25% on average annually between 2020 and 2022, compared with just 5% over the 2010-2020 period; meanwhile oil and gas companies’ R&D budgets were stable over 2010-2022. Beyond traditional energy companies – such as in aviation, rail, shipping, chemicals, cement and iron and steel – much lower shares of R&D budgets are typically spent on clean energy, indicating further opportunities to push clean energy innovation. The role of start-ups is also growing. Clean energy venture capital investments nearly doubled between 2010 and 2020, and then more than doubled again post-Covid-19, reaching USD 7 billion for early-stage and USD 35 billion for growth-stage start-ups in 2022, with notable increases in electric vehicles and batteries, renewables, and energy efficiency.

Venture capital investment in clean energy start-ups, 2010-2022

OpenFour priorities for decision makers

The rapid progress seen on certain clean energy technologies is an encouraging sign, suggesting the global clean energy innovation community will only get more vibrant by 2030. Recent technology developments are also creating new opportunities for entrepreneurs and countries seeking to position themselves in the new energy economy, especially in emerging and developing economies.

Yet sustained efforts will still be needed to get on track with net zero, and there are at least four priorities for decision makers:

- Stimulate innovation by fostering demand for clean energy, particularly in sectors where innovation needs are greater (e.g. heavy industry, long-distance transport), such as through public support, regulation and market incentives.

- Make pre-commercial technologies more bankable, especially in sectors where there are few clean energy options today. Contributing to fund prototyping and demonstration projects, supporting start-ups, and facilitating early-stage scale-up can share risks and improve the business case for technologies not yet on the market.

- Nurture a pool of innovators to generate diverse ideas, such as through funding for clean energy R&D and support for innovating institutions and companies. Even if net zero CO2 emissions could be met without major discoveries, embracing the uncertainty and potential for radically new ideas as well as spillovers is important to address future challenges.

- Foster international collaboration on clean energy innovation to share good practice approaches, learnings and resources, building on existing multilateral initiatives such as the IEA Technology Collaboration Programme and Mission Innovation. Large-scale demonstration projects, in particular, can benefit from stronger collaboration.

Reaching net zero emissions demands faster innovation, but we’ve already come a long way

Araceli Fernandez Pales, Head of Technology Innovation Unit

Simon Bennett, Energy Technology Analyst Commentary —