Cite report

IEA (2023), Energy Technology Perspectives 2023, IEA, Paris /reports/energy-technology-perspectives-2023, Licence: CC BY 4.0

Report options

Clean energy supply chains vulnerabilities

Highlights

The production of critical minerals is highly concentrated geographically, raising concerns about security of supplies. The Democratic Republic of Congo supplies 70% of cobalt today; the People’s Republic of China (hereafter “China”) 60% of rare earth elements (REEs); and Indonesia 40% of nickel. Australia accounts for 55% of lithium mining and Chile for 25%. Processing of these minerals is also highly concentrated, with China being responsible for the refining of 90% of REEs and 60-70% of lithium and cobalt. China also dominates bulk material supply, accounting for around half of global crude steel, cement and aluminium output, though most is used domestically.

Concentration of the largest manufacturers in global manufacturing capacity and material production, 2021

OpenChina is the leading global supplier of clean energy technologies today and a net exporter for many of them. China holds at least 60% of the world’s manufacturing capacity for most mass-manufactured technologies (e.g. solar PV, wind systems and batteries), and 40% of electrolyser manufacturing. Europe is generally a net importer, with the exception of wind turbine components; about one-quarter of electric cars and batteries, and nearly all solar PV modules and fuel cells are imported, mostly from China. For solar PV, China supplies equipment directly to all markets except North America. The United States imports two-thirds of its PV modules, primarily from Southeast Asia, where Chinese companies have been actively investing.

Notes: Flows represent battery packs produced and sold into EVs. Sources: IEA analysis based on EV Volumes from Benchmark Mineral Intelligence and company announcements.

Recent supply chain disruptions resulting from the Covid‑19 pandemic and Russia’s invasion of Ukraine, combined with rapidly growing demand, have dramatically increased the cost of materials and energy. The average price of lithium was nearly four times higher in 2022 than in 2019, and twice for cobalt and nickel. Battery metal price hikes in early 2022 led to increasing battery prices – up nearly 10% globally relative to 2021 – after years of continuous decline. The price of solar PV-grade polysilicon, copper and steel all roughly doubled between the first half of 2020 and that of 2022. These increases contributed to pushing up the price of PV modules by 25% and that of wind turbines outside China by up to 20%.

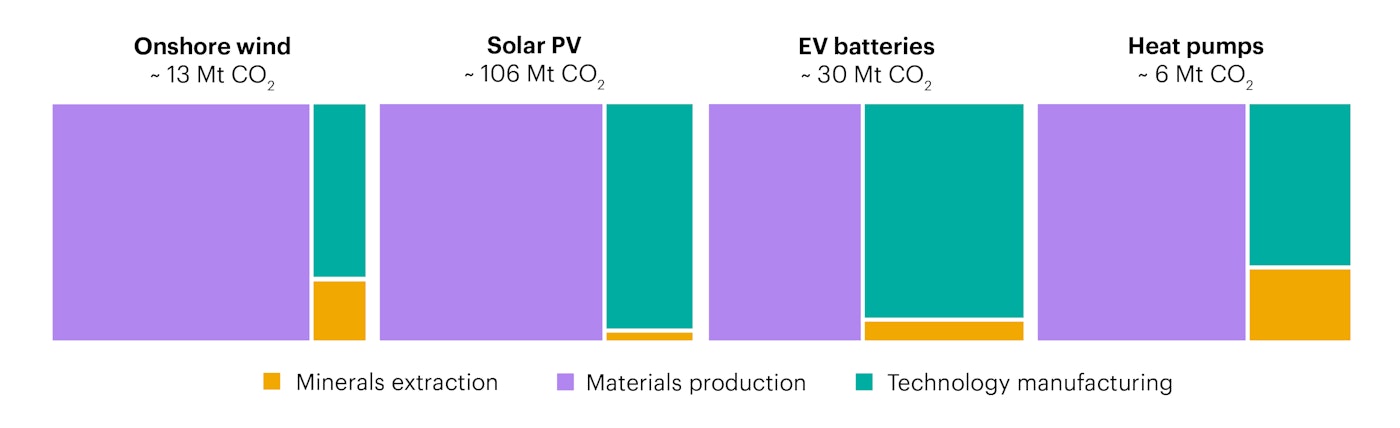

Clean energy technologies have far lower life-cycle CO2 intensities than their fossil counterparts, but their supply chains are still an important source of CO2 emissions and other pollutants. Material production and technology manufacturing typically account for over 90% of the emissions for the clean energy technology supply chains analysed. Reducing emissions from these steps is challenging, given the current lack of commercially available low-emission technologies in many cases, but an important undertaking in the transition to net zero emissions.

Total CO2 emissions from the production of solar PV, wind turbines, EVs and heat pumps by supply chain step, 2021

Open

{kind=link}