Cite report

IEA (2023), Global EV Outlook 2023, IEA, Paris /reports/global-ev-outlook-2023, Licence: CC BY 4.0

Report options

Policy developments

Introduction

Global electric vehicle (EV) markets today differ widely, shaped by different levels of policy support, corporate activity, consumer preference and awareness, driving patterns and cultural specificities. The role of policy has been particularly significant in steering corporate strategy towards electrification and enabling consumer uptake.

In today’s major EV markets – including China, Europe and the United States – early adoption was jump-started in many cases by policies to spur demand, such as vehicle purchase incentives. Direct incentives for carmakers were also used in China. Many of these countries and regions are now seeing EV markets maturing, especially for cars, for which sales shares are increasing rapidly. More developed markets such as China and several European countries are now progressively decreasing or phasing out incentive schemes for electric cars and shifting focus towards other segments such as heavy transport and charging.

At the same time, some governments in major markets have increased their targets for EV adoption further and are working to address other parts of EV supply chains, such as through policy support for vehicle and battery manufacturing and critical mineral supply chains. Many other countries outside the major markets have also started to introduce policy to support EV adoption in recent years, for the first time in some cases. Overall, global spending by governments and consumers on electric cars has significantly increased in the past few years, exceeding USD 400 billion in 2022.

For companies, policy requirements were an important driver for electrification in the early years of EV adoption. With the exponential growth of electric car sales, however, it has become increasingly important for major incumbent carmakers to offer EVs as a key part of their portfolios in order to capture market share and maintain a competitive edge. Competition is increasing, with a growing number of new entrants, particularly from China but also from other emerging market and developing economies (EMDEs), pushing the entire industry to accelerate decarbonisation. Overall, corporate strategy among major carmakers is shifting, and – as in recent years – 2022‑2023 saw a series of important EV announcements: fully electric fleets, cheaper cars, more investments, and integration with battery making and critical minerals.

This section of the Outlook provides information on selected policy developments announced between April 2022 and March 2023, since the last edition of the IEA Global Electric Vehicle Outlook in 2022.1

As in recent years, most policies supporting EVs target the electric light-duty vehicle (LDV) segment, for which market maturity is most advanced and vehicle availability greatest. In 2022, more than 90% of global sales of LDVs were covered by policy that encourages EV uptake. Typical policies include fuel economy and pollutant standards; zero-emission vehicle mandates; economic and budgetary regulation for fuels and vehicles, such as through fiscal regimes and taxation; purchase incentives and subsidies; and bans on internal combustion engine (ICE)-only vehicles.

There is an increasing policy focus on the heavy-duty vehicle (HDV) segment, including medium freight trucks, heavy freight trucks and buses, and almost 70% of global HDV sales are now covered by EV policies. Countries are increasing funding, committing to zero-emission vehicle2 (ZEV) deployment targets and enacting HDV-specific policies for the first time. In 2022, 11 countries signed on to the Global Memorandum of Understanding (MoU) on Zero-Emission Medium- and Heavy-Duty Vehicles, bringing the total number of signatories to 27. These countries aim for 100% zero-emission new truck and bus sales by 2040.

Policies are also shifting towards electric vehicle supply equipment (EVSE), or charging, and currently almost 80% of global EV sales (LDV and HDV) are covered by EVSE-related policy. Countries are increasingly dedicating funds to EVSE deployment, acknowledging that lack of charging infrastructure can be a critical barrier to EV adoption.

The 2022-2023 period was notable for the announcement of policies in the European Union and United States – new CO2 standards and the Inflation Reduction Act (IRA), respectively – which are expected to have a significant impact on the pathway to zero-emission road transport. In addition, several EMDEs outside China have developed specific industrial policy to support battery and EV production, seeking to capitalise on opportunities to strengthen domestic manufacturing capacity.

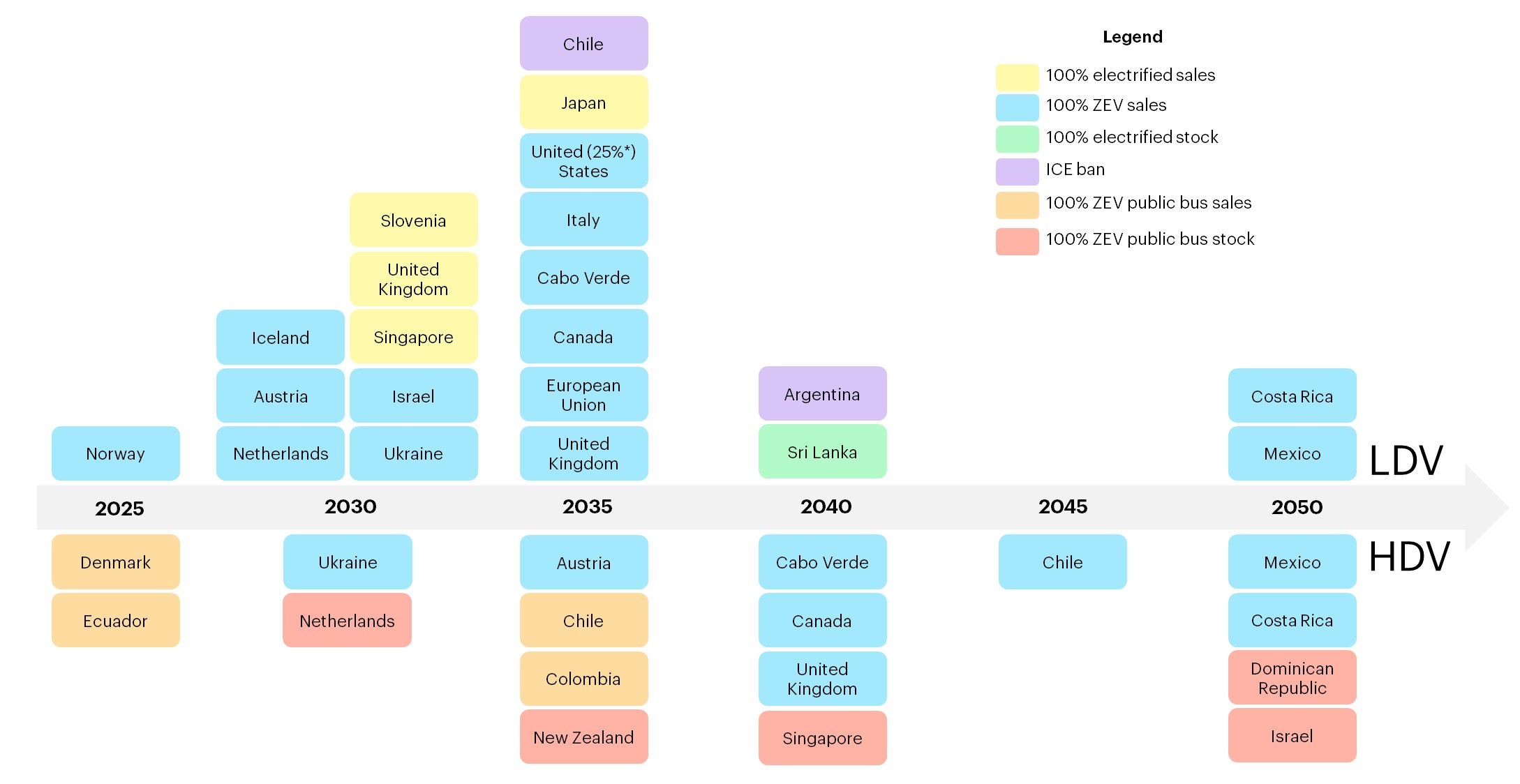

Zero-emission vehicle targets are a cornerstone of policy for transport decarbonisation, and almost all such targets, with respect to market coverage, have relatively short- to medium-term implementation dates. For LDVs, around half of annual global sales are covered by targets for 2035 or earlier, increasing only slightly to 55% by 2050. While the vast majority of this coverage comes from China, the European Union and the United States, there are promising increases in ambition in other markets.

Global zero-emission vehicle mandates and internal combustion engine bans

Open{kind=link}

Policy to develop EV supply chains

Policy increasingly aims to boost manufacturing, not just deployment

Several of the policies announced in 2022 and early 2023 relate to the development of EV manufacturing in addition to EV deployment.

In China, the largest market for electric cars, supporting EV manufacturers and companies through direct incentives along EV supply chains to ramp up domestic production is not a new phenomenon. The past decade has seen a sustained use of supply- and demand-side incentives for domestic firms, as well as joint ventures with international carmakers. Support has been particularly prevalent at the local level in China, thereby stimulating national uptake and the development of several major EV companies. Regions and cities have also recently announced targets for manufacturing, such as Chongqing’s goal to produce and sell more than 10% of China’s new energy vehicles (NEVs),3 and Jilin’s aim to reach an annual production capacity of around 1 million NEVs, both by 2025, supported by policies focusing on EV manufacturing.

There were also notable announcements in other major markets, such as the IRA in the United States, and the Green Deal Industry Plan in the European Union. In India, the aims of the national Production Linked Incentive (PLI) scheme to encourage domestic EV manufacturing have also been supported by subnational government, such as in Tamil Nādu, where updated policy encourages local EV manufacturing. A number of other examples in EMDEs further demonstrate this trend, such as in Indonesia, which has introduced policy to invest in battery manufacturing, and Ethiopia, which is offering tax exemptions for locally assembled EVs in order to attract investment. In July 2022, Morocco announced plans to build a large EV battery factory, and the country marked the completion of its first domestically produced battery electric vehicle (BEV) in December 2022 following the reduction of tariffs on lithium-ion cells in 2021 to encourage assembly.

United States: Inflation Reduction Act

The Inflation Reduction Act (IRA), passed in August 2022, includes various tax incentives and funding programmes to meet the aim of building a clean energy economy. Part of the Act concentrates on accelerating EV adoption, with dedicated funding drawn from the USD 369 billion allocated for climate investments.

The Clean Vehicle Tax Credit introduces a new set of conditions for EV models to qualify for incentives. From 2023 onwards, these conditions stipulate that final assembly must occur in North America, and that vehicles must have a 7 kWh battery or greater (to exclude low-range plug-in hybrid electric vehicles [PHEVs]), be under 6.35 t gross vehicle weight (GVW), and have a suggested retail price of less than USD 80 000 for vans, SUVs and pickup trucks, or USD 55 000 for other vehicles. In order to qualify for the incentive, the EV buyer’s household income must be below the limit set by the US Internal Revenue Service. These conditions open eligibility for an incentive of up to USD 7 500 per vehicle: USD 3 750 if the battery meets the critical mineral requirement, and another USD 3 750 if it meets the component requirement.4 Furthermore, from 2025, vehicles with any critical minerals from “foreign entities of concern” will not be eligible for the credit, and vehicles with battery components from such entities will be ineligible from 2024.

Several of the major US automotive manufacturers have submitted a list of specific models that comply with the new requirements, and removing the manufacturer sales cap of 200 000 means GM and Tesla can participate in the scheme. Of the 37 models listed, 4 are PHEVs and 33 are BEVs. The average listed retail price for the eligible PHEVs and BEVs is just below the USD 55 000 and USD 80 000 limit for cars and SUVs, respectively, indicating original equipment manufacturer (OEM) corporate strategy to meet the eligibility criteria of the IRA, even if this implies cutting prices in some cases. The Act also commits USD 1 billion to incentives and infrastructure projects for HDVs between now and 2031.5 For vehicles from approved manufacturers, with 15 kWh or more of battery capacity, the tax credits are up to USD 40 000 per vehicle.

In addition to demand-side credits for vehicle purchase, the IRA includes supply-side Advanced Manufacturing Production Tax Credits. Under this scheme, the US government provides subsidies for domestic battery production of up to USD 35 per kWh, plus another USD 10 per kWh for module assembly. Assuming average battery prices in 2022 are around USD 150 per kWh, these new US production incentives could account for nearly a third of total battery price.

Finally, in addition to confirming that countries with existing free trade agreements have preferred status as suppliers, the United States signed an MoU with the Democratic Republic of Congo and Zambia in January 2023, committing to support development of a productive supply chain from mining to assembly.

European Union: Green Deal Industry Plan

In February 2023, the European Union presented the Green Deal Industrial Plan, which has four pillars related to progress on net zero-related projects: faster permitting, financial support, enhanced skills, and open trade. The plan also includes provision for the creation of a Critical Raw Materials Act, the proposal for which was issued in March 2023, with a focus on security of supply, extraction and environmental standards, as well as recycling.

The faster permitting for facilities, including battery production, will be formalised via the proposed Net Zero Industry Act, providing simplified and predictable planning approvals. As well as loosening rules on state aid until 2025, the financial support package of the plan attempts to allow faster access to essential subsidies and loans, to compensate businesses for high energy prices, to help ensure liquidity, and to reduce electricity demand. The plan also aims to reskill workers affected by the green transition, and to establish Net Zero Industry Academies. Lastly, the trade element focuses on improving the resilience of the EU’s supply chains, opening trade with new partners and attracting private investment.

In March 2023, the European Union proposed the Net Zero Industry Act, which aims to meet 40% of the European Union’s needs for strategic net zero technologies with EU manufacturing capacity by 2030. These technologies explicitly include battery and storage technologies, and for batteries the aim is for nearly 90% of the European Union’s annual battery demand to be met by EU battery manufacturers, with a combined manufacturing capacity of at least 550 GWh in 2030, in line with the objectives of the European Battery Alliance. These announcements came just as CO2 standards for car sales over 2030-2035 tightened under the Fit for 55 package.

India: Production Linked Incentives (PLI)

The Indian PLI on Advanced Chemistry Cell (ACC) Battery Storage was announced in late 2021 with the aim of boosting domestic battery manufacturing with a budget of INR 181 billion (Indian rupees) (USD 2.2 billion). Specifically, the government aimed to reach a cumulative 50 GWh in domestic manufacturing capacity by allocating funding to companies based on the sales of batteries manufactured in India, disbursed over five years, and dependent on meeting a domestic value-add of at least 25% in year 1, increasing to 60% in year 5. This is particularly ambitious given that there is currently no significant domestic battery cell manufacturing in India, and the 50 GWh figure is 50% greater than anticipated domestic demand as projected in the IEA Stated Policies Scenario (STEPS) in 2025. The scheme attracted 10 bids with cumulative capacity of 128 GWh in early 2022, and by July 2022, the government had assigned funding to 3 companies – Reliance, Ola and Rajesh – for a total of at least 30 GWh of battery manufacturing capacity with the remainder to be allocated to the next highest placed bidder(s). Other private companies are expected to establish an additional 95 GWh.

The Automobile and Auto Component PLI scheme has two parts: the Champion OEM incentive scheme, which grants incentives for sales of advanced automotive technology vehicles (battery electric and hydrogen fuel cell vehicles) across all vehicle segments; and the Component Champion scheme, which provides incentives for sales of certain components for both ICE and electric vehicles. The budgetary outlay is INR 260 billion (USD 3.2 billion) over five years, and the scheme has been successful in attracting investments worth INR 677 billion (USD 8.3 billion), which will be spent over a period of five years. A total of 95 applicants had been approved under this scheme as of March 2022. In both schemes, the minimum domestic value-add requirement is 50%.

Leveraging critical mineral resources to build domestic manufacturing

Recognition of the vital role of critical minerals in the EV transition has also catalysed policy action. As carmakers and battery manufacturers around the world race to secure supply as EV demand increases, governments are seeking to position themselves in global supply chains, with a focus on increasing domestic capacity. It will be important to ensure these new supply chains for critical minerals are ethical and environmentally sustainable into the future.

The European Union’s December 2022 proposed revisions to the EU Battery Directive introduce new rules for the production, recycling, and repurposing of batteries. The European Union also proposed the Critical Raw Materials Act in March 2023, which aims, by 2030, to achieve extraction capacity of 10% of the European Union’s annual consumption of strategic raw materials; processing capacity for 40%; and recycling capacity for 15%. Objectives also include diversifying the origin of imported materials to increase supply chain security and resilience, and improving the environmental sustainability of mineral-related activities.

In the United States, the importance of critical minerals and the preference for developing domestic capacity has been underlined by the stipulation under the IRA that half of the vehicle subsidy is dependent on meeting the critical mineral requirement.

Initiatives to stimulate domestic manufacturing and ensure supply of critical minerals are also underway in many other countries. Australia is aiming to accelerate lithium production for both export and domestic downstream processing. Recent policy developments have included a consultation on the Australian Made Battery Plan, which sets out an AUD 100 million (Australian dollars) (USD 65 million) budget proposal for domestic battery manufacturing projects in Queensland, and on a new Critical Minerals Strategy. Like Chile, Australia has a free trade agreement with the United States, meaning greater synergy with the IRA than in countries not covered by such agreements. Argentina sees an opportunity to build a battery manufacturing industry that would create 2 500 jobs by 2030, and is considering the introduction of a domestic market quota of 5%, potentially increasing to 20%, to guarantee domestic industry access to lithium. Japan aims to increase domestic production of vehicle batteries to 100 GWh by 2030 under the Green Growth Strategy. In 2022, Japan earmarked JPY 331.6 billion (Japanese yen) (USD 2.5 billion) to develop materials for magnets and batteries to reduce the dependency on rare earth elements and lithium, including those used for EV applications. In Mexico, a decentralised public body, Lithium for Mexico, was created in August 2022, recognising lithium as strategic mineral and nationalising the value chain, with a target that 50% of vehicles produced in Mexico will be ZEVs by 2030. Russia is aiming to leverage minerals to develop a battery industry, and for no less than 10% of car production to be EVs in 2030.

In 2020-2021, India imported lithium-ion cells worth USD 1 billion, more than 95% of which were from Hong Kong and China, according to trade data. To reduce dependency on imports, in 2022 India issued Battery Waste Management Rules, which aim at recycling or refurbishing all types of batteries, including those of EVs. The rules also set the goal of increasing the recycled content of EV batteries to 20% by 2030, including for imported products. In February 2023, India announced its first inferred lithium deposits of 5.9 Mt.6 If confirmed, this may become a game-changer for India and for global cell manufacturing.

Other countries are also positioning themselves as potential players in the EV supply chain: In 2023, Iran claimed to have identified lithium reserves, which if confirmed could amount to 8.5 Mt, or the second largest such reserves in the world.

Policy support for electric light-duty vehicles

New EU standards introduce deadlines and increase targets

Over the past year there has been substantial progress towards adopting legislation in line with reducing emissions in the European Union by at least 55% by 2030, as outlined in the Fit for 55 package. In March 2023, the European Union adopted new CO2 standards for cars and vans requiring a 55% and 50% reduction in emissions of new cars and vans by 2030 (compared to 2021), and 100% for both by 2035. As stated in the regulation, the Commission will also submit a proposal to allow for the registration of vehicles running exclusively on CO2-neutral e-fuels after 2035.

In June 2022, the European Parliament also called for amendments to regulations regarding the default utility factor for PHEVs, which represents the share of distance travelled using the battery compared to the distance travelled using the ICE. Consequently, from 2025 the utility factor (with its effect on vehicle emissions) will be based on the 2022 ICCT-Fraunhofer study of real-world data rather than estimates, substantially increasing the assumed emissions. This is expected to significantly decrease the incentive for carmakers to use PHEVs to meet European fleet targets. As of 2027, the updated methodology will be based on an even split of private and company cars, as the latter have been responsible for an even greater gap between assumed and actual performance. Furthermore, it is proposed that from January 2027 the utility factor will be changed to reflect the latest results of on-board fuel consumption monitoring devices.

Tighter Euro 7 regulations expand coverage of emissions

In November 2022, the European Commission proposed new Euro 7 emissions standards for cars, vans, trucks and buses. The proposed emission standards are intended to be more reflective of real driving conditions, particularly city driving, and regulate not just tailpipe emissions, but also emissions from brakes and tyres – including for EVs. The standards are also intended to reinforce new stricter air quality standards proposed in October 2022.

As with the United Nations regulations (see “Globally harmonised technical regulations for safer and cleaner electric vehicle deployment”), the Euro 7 emissions standards would introduce minimum performance standards for LDV battery durability of 80% by year 5 or 100 000 km, and 70% from years 5 to 8 or 160 000 km.7 Also included are nitrogen oxide (NOx) emissions reductions of 35% for LDVs and 56% for HDVs, and tailpipe particle emissions reductions of 13% for LDVs and 39% for HDVs. These limits cannot be exceeded before 200 000 km or 10 years of driving, double the previous requirements. They represent an anticipated cost increase of EUR 90 to 150 (USD 95 to 160) for LDVs, and EUR 2 600 (USD 2 750) for HDVs compared to Euro 6/VI.

Greater ambition for US states under Advanced Clean Cars II

In November 2022, the California Air Resources Board approved the Advanced Clean Cars II (ACC II) rule, which sets a minimum ZEV sales shares for passenger LDVs ranging from 35% in 2026 to 100% in 2035.8 Any vehicle sold from 2035 onwards must be a zero-emission vehicle or PHEV. This follows sustained support for low- and zero-emission vehicles in California in the past decades, such as through the zero-emission vehicle credits. While the regulation can only take effect after a waiver is granted to California by the US Environmental Protection Agency, other states have already followed California’s lead. Vermont, Washington, Oregon and New York have all adopted ACC II, altogether representing about 20% of US passenger LDV sales. Currently, Massachusetts, Delaware and Colorado have also either begun the process to adopt ACC II or have announced intentions to do so, which would bring the share of sales covered by the rule to almost 25%.

National plans in many countries pave the way for zero-emission car transport

In 2022-2023, more and more countries proposed policy to accelerate electric car adoption, either by strengthening existing plans or introducing a support mechanism for the first time.

In Europe, the United Kingdom brought forward the date to end the sale of fully ICE cars and vans to 2030, five years earlier than previously announced, with a full transition to 100% ZEV sales by 2035.9 In March 2023, the government laid out proposed ZEV sales share trajectories for cars and vans to reach the 2035 target.

Greece, which had a previous target of 30% ZEV sales share by 2030, strengthened its policy to only allow the sale of zero-emission LDVs from then onwards. In Switzerland a target first established in 2018 for a 15% electric car sales share by 2022 has been surpassed, reaching 25% in 2022, building on strong collaboration and investment across around 50 leading organisations through the Electromobility Roadmap. The new target stands at 50% electric car sales share by 2025. Italy’s subsidy scheme has also been renewed with a focus on scrapping older, more polluting ICEs, similar to a scheme in Singapore. Spain has a similar focus on scrappage, accompanied by support for lower-income individuals. In Denmark, changes to taxation aim to make EV company cars more attractive, while in Finland, import and annual taxes for EVs have been significantly reduced. Austria renewed its EV subsidy in 2023, applying the same rates as the previous year.10 Croatia and Cyprus11 both began subsidising EV purchase in 2022.

In 2022, Canada increased its national ambition for LDV deployment, with current goals to achieve a zero-emission sales share of 20% by 2026, 60% by 2030 and 100% by 2035. On the provincial level, British Columbia has increased its 2030 target to 90%.

Having funded a charging infrastructure programme since 2020, in February 2022 Australia also started providing competitive grant funding supporting the purchase of EVs (both light- and heavy-duty) for commercial use. The total funding amounts to AUD 128 million (USD 89 million) and is a component of the expanded AUD 500 million (USD 346 million) Future Fuels Fund. In May 2022, New Zealand published its first comprehensive emissions reduction plan. It aims for 30% of the LDV stock to be ZEVs by 2035. Electric cars accounted for over 10% of new sales in 2022, despite New Zealand only introducing a purchase subsidy in mid-2021. This also covers imports of used vehicles, given their prevalence in the country, as well as several non-purchase related incentives.

Japan's Green Growth Strategy, announced in 2021, sets targets to reach 100% electrification of LDV by 2035, and the 2023 Act on the Rational Use of Energy tracks and accelerates the targets set under the Strategy.

In EMDEs, governments are also increasing ambition. EVs are viewed as an opportunity to reduce air pollution, mitigate climate impacts and decrease reliance on energy imports. The EV policies being introduced commonly take the form of tax exemptions for EVs, equipment and parts, as well as purchase incentives, mandates, and deployment targets.

In Indonesia, government vehicles have been required to be electric since 2022, and EV purchase subsidies have been put in place from 2023. In Seychelles, the aim is for 30% of new vehicles sales to be electric by 2030 and the forthcoming National Electric Mobility Strategy will contain a target of 100% of buses to be electric by 2050. In Panama, 40% of the stock of selected public vehicles are to be EVs by 2030. Viet Nam has introduced a net zero emissions target for the transport sector in 2050, aiming to use vehicles powered by 100% electricity and green energy, with a ban on the production, assembly and import of fossil fuel-powered vehicles in 2040. Ghana’s recently released strategy contains a target that 4%, 16%, and 32% of new sales are to be EVs in 2025, 2030, and 2050, respectively. In addition, countries recently proposing tax-related policies include Angola, Brazil (following previous tax exemptions for imports of electric cars dating back to 2015), Ecuador, Pakistan, Trinidad and Tobago, Tunisia, Uzbekistan, and Viet Nam.

China: local action ramps up as national subsidies phase out

In China, December 2022 saw the end of the national NEV subsidy scheme, originally aimed for phase-out two years earlier, and following a gradual reduction of national subsidies for NEV purchases since 2017. Meanwhile, with a sales share of almost 30% in 2022, China’s NEV market has surpassed the country’s target of a 20% sales share by 2025. The extended vehicle purchase tax exemption for NEVs will remain as the main national-level financial incentive until the end of 2023.

Moreover, road transport electrification is stated as a goal in multiple guiding strategies. To reduce air pollution, China aims to reach a 50% NEV sales share by 2030 in its “key air pollution control regions”, which combined account for nearly 80% of China’s car market. In addition, China’s national action plan to reach carbon peaking before 2030 sets out a target for the sales share of NEVs to reach around 40% by 2030.

Meanwhile, targets and favourable policies at the regional level continue to play an important role. In line with the country’s national action plan, 18 Chinese provinces currently have explicit NEV targets as part of carbon peaking policies, aiming for 40% of NEV sales share by 2030, with Tianjin at 50%. Regional sectoral strategies and local 14th Five-Year Plans also set more ambitious targets in some cases, such as Shenzhen’s aim to achieve a 60% NEV sales share by 2025, and Shanghai’s BEV sales share target of 50% by 2025. Several regional governments announced local incentives at the beginning of 2023; for example, Zhengzhou and Wuxi are providing vouchers for NEV purchases, while Beijing and Shanghai both announced incentives to replace an ICE vehicle with a NEV.

The focus and level of incentives are changing as markets mature

- In 2023, Norway reintroduced value-added tax (VAT) on EVs costing more than NOK 500 000 (Norwegian kroner) (USD 52 000), meaning only the most expensive models would see price increases. Norway proposed to replace the VAT exemption with a new subsidy scheme, though few details have been released to date. Other advantages and incentives have also been gradually reduced.

- In the United Kingdom, subsidies for electric cars ended in 2022, having exceeded a 20% sales share, after the available grant was gradually reduced between 2016 and 2021.##anchor12## Subsidies remain in place for electric taxis, vans and trucks, as well as for company cars with new tax exemptions, and the focus on charging is also increasing.

- Germany and Ireland both lowered purchase incentive levels in 2023.

- The Netherlands has been reducing premiums year-on-year, with a EUR 400 (USD 420) reduction between 2022 and 2023.

- Sweden had first planned to tighten the cap on purchase incentives for electric cars from SEK 70 000 (Swedish kronor) (USD 7 000) in 2022 to SEK 50 000 (USD 5 000) in 2023, following an increase from SEK 60 000 (USD 6 000) in early 2021. Then, in light of closer price parity between electric and ICE cars, Sweden announced that the purchase incentive would expire from November 2022 onwards.

- After increasing the incentive in order to boost sales during the Covid-19 pandemic, France reduced incentives from EUR 7 000 (USD 7 400) in 2021 to EUR 6 000 in 2022 (USD 6 300) and EUR 5 000 in 2023 (USD 5 300). However, the purchase incentive for lower-income households was increased from EUR 6 000 (USD 6 300) in 2022 to EUR 7 000 (USD 7 400) in 2023 in order to improve equity of access to EVs.

- In Korea, the government promotes EVs by applying higher subsidy amounts to vehicles with greater fully electric range. The maximum passenger car incentives slightly decreased from KRW 7 million (Korean won) (USD 5 400) to KRW 6.8 million (USD 5 300) in 2023, though consumers can benefit from local subsidies as well. For electric LCVs, the incentives per vehicle decreased from KRW 14 million (USD 10 800) to KRW 12 million (USD 9 300) in 2023. However, with around 30% more passenger cars and commercial vehicles subsidised, total government funding for electric LDV subsidies increased from KRW 1 561 billion (USD 1.2 billion) in 2022 to KRW 1 676 billion (USD 1.3 billion) in 2023. Additionally, in April 2022, Korea ended their policy of free light commercial vehicle (LCV) registration, yet has remained a leader in electric LCV deployment in 2022, averaging 27% of sales over the year.

- In 2022, Japan increased their EV subsidy scheme to JPY 70 billion (USD 530 million) – doubling support for BEV purchases up to JPY 850 000 (USD 6 500) and JPY 550 000 (USD 4 200) for PHEV.

Stronger policy preference for fully battery electric options

Recent developments indicate possible strengthening of policy support for battery electric cars over PHEVs. In Europe, for example, Belgium, Finland, the Netherlands, Portugal and the United Kingdom supported BEVs over the 2019-2022 period, but not PHEVs. In 2022, Ireland decided to end subsidies for PHEVs, followed in 2023 by Germany.

In China, Shanghai offers purchase subsidies for BEVs but not for PHEVs, and several Indian states have set BEV-specific targets without including PHEVs. The United States and Canada have maintained the same level of support for PHEVs since 2019. In California, however, a 40 mile (65 km) minimum fully electric range is being introduced for PHEVs. The IRA is now also stipulating a minimum of 7 kWh battery capacity to qualify for subsidies, thereby excluding low-range PHEVs.

Policy support for electric heavy-duty vehicles

New EU CO2 standards for trucks and buses could be a step-change

The European Commission released proposed revisions of the regulation on HDV emissions in February 2023. The scope of the proposed regulation includes smaller trucks, city buses, long-distance buses, and trailers, to cover 95% of sectoral emissions, up from about 70% currently. This demonstrates a step-up in ambition: the International Council on Clean Transportation (ICCT) estimates that the new regulations could achieve sectoral emissions reduction of over 75% by 2050 relative to 2020.

The revisions would increase targets for CO2 emissions reductions to 45% by 2030 relative to 2019, 65% by 2035, and 90% by 2040. Furthermore, all city buses should be ZEVs by 2030. Compliance will be measured separately for passenger (bus and coach) and freight vehicles via a system of credits and debts settled at the end of five-year periods between 2025 and 2040. Additionally, the definition of ZEV applied is changing, increasing from 1 gCO2 per vehicle-km to 5 gCO2 per tonne-km (tkm) to allow for dual fuel. Trading between economically linked entities (e.g. between brands at the same parent company) is allowed to help meet targets. The minimum range of long-haul trucks is defined as 350 km, and financial penalties are applied for non-compliance.

Several European Union member countries are strengthening support for zero-emission heavy transport in national plans. Germany has among the highest truck purchase subsidies in Europe, with 80% of additional costs of the vehicle and/or the charging infrastructure covered. Ireland’s updated Climate Action Plan includes a target of 700 low-emission heavy-duty trucks by 2025, a 30% zero-emission heavy-duty truck sales share by 2030, and provisions for HDVs. Ireland also introduced its first electric bus target: 300 by 2025. In Denmark, from 2025 onwards, taxes on trucks will be based on CO2 emissions, sending a clear policy signal to operators. In April 2022, Italy made subsidies available for trucks between 3.5 and 12 t, and in the same month, the Netherlands introduced a wide-ranging scheme covering vehicles from small trucks up to tractor units (4.25‑18+ t). Croatia implemented a scheme with a similarly wide scope in June. In total, ten European countries now also have a subsidy scheme for HDVs, five of which were introduced in 2022/23.

Increasing inclusion of HDVs in targets and policy incentives

In the United States, the IRA provides USD 1 billion for vehicles and infrastructure specifically for HDVs, including subsidies, and the state of California’s funding package for charging infrastructure will see 70% of funds dedicated to charging for HDVs. In the United Kingdom, HDVs remain included in subsidy schemes even though support for electric cars has been phased out. Similarly, Australia’s subsidy scheme under the Future Fuels Program specifically targets HDVs and HDV charging with dedicated funding that is not available for LDVs.

Several countries have specific targets for zero- or low-emission heavy transport. In New Zealand, the aim is to reduce emissions from freight transport by 35% by 2035. Norway aims for virtually zero-emission goods distribution by 2030 in the biggest urban centres. Tianjin (China), aims to have 80% NEVs in public transport, rental, logistics and delivery vehicle sales by 2025, while Viet Nam’s net zero transport by 2050 goal includes HDVs. Japan aims to introduce 5 000 electric HDVs by 2030, with a JPY 13.6 billion (USD 120 million) plan to electrify HDVs and taxis. Some countries are also introducing financial support for electric truck purchases for the first time. In July 2022, Canada’s Incentives for Medium- and Heavy-duty Zero-Emission Vehicles (iMHZEV) programme began to offer incentives up to CAD (Canadian dollars) 200 000 (USD 160 000) towards the purchase or lease of ZEV trucks of various categories.

With respect to electric buses, overall model availability is higher and cost-competitiveness better than trucks, making them generally more affordable. Indeed, several EMDEs have begun including ambitious deployment targets for electric buses in national plans, often ahead of LDV targets. For example, in April 2022, Panama announced the aim of transitioning towards electric public transport, reaching a 10% share by 2025, 20% by 2027, and 33% by 2030. In February 2023, Tamil Nādu in India also introduced a target for 30% of their bus fleet to be electric by 2030 as part of a broad strategy to promote EVs and supporting infrastructure. In advanced economies, grants for electric buses have been introduced in Canada. The United States also provides substantial funding towards the purchasing or leasing of electric buses: up to 85% of vehicle costs and up to 90% of infrastructure costs.

Heavy-duty vehicle policy coverage in selected key countries

Open

{kind=link}

Policy support for EV charging infrastructure

Support is gradually shifting from vehicles to charging in some markets

In countries where electromobility is more well developed, focus is shifting towards supporting charging infrastructure and moving away from more expensive private vehicle subsidisation. In the United Kingdom, for example, in June 2022 the government announced its intention to refocus on charging, after winding down the electric car subsidy programme. Almost GBP 1.6 billion (USD 2.1 billion) of government funding has been committed to supporting the EV Infrastructure Strategy, which set an expectation of 300 000 public chargers being installed by 2030. The UK government is also working to increase the availability of on-street chargers, particularly in residential areas where off-street parking is not available.

With charging identified as the top consideration for consumers in China, Guangdong, Hunan and Shanghai, among other regions, have implemented subsidies for the deployment of charging points. Shenzhen is targeting 43 000 fast chargers and 790 000 slow chargers by 2025, and Chongqing 240 000 chargers.

Germany, which is also winding down its vehicle subsidy scheme, has at the same time supplemented the budget for fast chargers. In Switzerland, the government extended its Electromobility Roadmap in 2022, with the goal of achieving 20 000 public charging stations by 2025 to support the 50% EV sales share target. Having launched a vehicle subsidy scheme in 2021, Poland is now also subsiding charging infrastructure. Finland and Denmark have recently committed to greater support of charger roll-out, as has Ireland, which released a revised ZEV plan that focuses on public charging.

Additional support for charging infrastructure aims to service different road transport segments in more settings

Some countries are choosing to fund infrastructure development in advance of large-scale adoption of EVs. One notable example is Australia, which has had grants to fund charging prior to 2020 and a dedicated infrastructure funding programme since 2020, and began to provide support for electric HDVs in 2022, in conjunction with charging. 13 The first period of Viet Nam’s strategy includes building a charging network, without a focus on subsidising vehicles. Similarly, Bulgaria’s efforts to promote EVs are starting with charging. In India, targets and incentives are being developed at the state level to supplement national ambitions, with the Tamil Nādu government set to subsidise the installation of 750 chargers. Under the Green Growth Strategy, Japan plans to construct 150 000 publicly accessible charging stations by 2030: 30 000 of which will be fast charging.

In the United States, more than USD 1.5 billion has been approved under the National Electric Vehicle Infrastructure (NEVI) Formula Program to help build EV chargers covering approximately 75 000 miles of highway across the country. National standards to qualify for the funding were adopted in 2023 with the aim of creating a convenient, affordable, reliable, and equitable network of chargers throughout the country. These standards will harmonise payments and pricing information for charging, and aim to ensure minimum numbers and types of chargers, including fast charging, to support achievement of the target of installing 500 000 chargers no more than 80 km apart along major routes by 2030. In addition, under the IRA, as of January 2023, vehicle charging infrastructure installations are eligible for a tax credit of up to USD 100 000, and consumers who

purchase a home charger can receive a tax credit of up to USD 1 000. California, often a front-runner in EV policy development, committed additional funding of USD 1 billion of funding to charging infrastructure in November 2022. Both at a national level and under California’s funding scheme, there is financial support to build out medium- and heavy-duty truck charging stations.

Canada recently increased funding available through the Zero Emission Vehicle Infrastructure Program by an additional CAD 400 million (USD 310 million) to extend the programme through March 2027. The programme supports the deployment of public and private chargers, including at multi-unit residential buildings and workplaces, as well as funding strategic infrastructure projects for urban delivery and fleet applications. Furthermore, the Canada Infrastructure Bank announced in 2022 that it will invest CAD 500 million (USD 385 million) in large-scale charging infrastructure. This is all to support the government’s target of 84 500 chargers deployed by 2029.

In 2021, the European Commission proposed the Alternative Fuels Infrastructure Regulation (AFIR) in place of the 2014 Directive. As of March 2023, the European Council and European Parliament have a provisional agreement for the AFIR, which includes requirements for total power capacity based on the size of the light EV fleet, and coverage requirements for the trans-European network-transport (TEN-T) with respect to light- and heavy-duty vehicles. An agreement between the European Investment Bank and the European Commission will make over EUR 1.5 billion available by the end of 2023 for alternative fuels infrastructure, including for EV charging. Grants to support EVSE deployment are also available from the Connecting Europe Facility (CEF) for Transport programme.

International initiatives and pledges

Accelerating to Zero

The overarching goal of the Accelerating to Zero (A2Z) coalition launched at the Conference of the Parties (COP 27) is for all sales of new cars and vans globally to be ZEVs by 2040, and by no later than 2035 in leading markets. The coalition builds on the Zero-Emission Vehicles Declaration, which received some 130 signatures on launch at COP26, and now has 223 signatories. These include 30 governments in advanced economies,14 11 governments in EMDEs,15 73 local/regional governments, 14 automotive manufacturers, 47 fleet owners and operators, 15 investors with shareholdings in automotive manufacturing, 2 financial institutions and 31 other signatories. The 40 governments together accounted for almost a quarter of annual LDV sales worldwide, and close to 20% of electric LDV sales in 2022. Some subnational government or non-governmental signatories have also set specific, more ambitious goals, such as regional or city authorities and fleet owners and operators aiming to electrify their fleets by as early as 2030.

Zero-Emission Government Fleet Declaration

In 2022, recognising the catalytic role that national governments can have via demand signals and leadership, a group of nine countries16 committed to the Zero-Emission Government Fleet Declaration. They aim to reach 100% zero-emission cars and vans in government fleets, with an additional aspiration of 100% zero-emission trucks and buses, by no later than 2035. Exact timelines vary by country. For example, 75% and 100% of acquisitions should be electric by 2025 in Australia17 and Israel, respectively; 100% of acquisitions by 2027 in the United States; and 100% of the LDV stock should be zero-emission by 2030 in Canada.

Zero-emission Vehicle Emerging Markets Initiative

In 2022, at COP27, the World Business Council for Sustainable Development (WBCSD), the United States and the United Kingdom launched the Zero-Emission Vehicle Emerging Markets Initiative. It aims to enhance co-operation between public and private actors in EMDEs to accelerate the transition to zero-emission road transport. Specifically, the initiative opened a dialogue between governments and corporates on public support and private investment to achieve ZEV deployment targets in EMDEs, with the view to facilitate and announce agreements at COP28. It gathers companies that have announced a combined USD 50 billion in investment and committed to deploy over 2 million EVs in EMDEs by 2030. In February 2023, the first dialogue of the series took place in India, launching a country pilot programme there.

Global Memorandum of Understanding on Zero-Emission Medium- and Heavy-Duty Vehicles

In 2021, the Dutch government and Drive to Zero programme launched the Global Memorandum of Understanding (MoU) on Zero-Emission Medium- and Heavy-Duty Vehicles, through which signatories commit to work together to achieve 100% ZEV bus and truck sales by 2040, with an interim goal of 30% by 2030. In 2022, Aruba, Belgium, Croatia, Curaçao, Dominican Republic, Ireland, Liechtenstein, Lithuania, Sint Maarten, Ukraine, and the United States all signed the MoU. This brings the total number of countries and territories among the signatories to 27,18 accounting for over 15% of total annual sales of new medium- and heavy-duty vehicles worldwide. The MoU also has endorsements from regional government, manufacturing, fleet owners and operators, among others.

Greening Corporate Fleets

The European Commission committed to promote commercial use of zero-emission vehicles through a Greening Corporate Fleets initiative in 2023. In an open letter to the Commission shared by Transport & Environment, a campaign group, 30 private and state-owned companies, as well as industry groups, called for the Commission’s initiative to include a binding target that by 2030 all new corporate LDVs should be ZEVs. The companies include fleet owners and operators and EV infrastructure developers.

The letter was also signed by the EV100 campaign, which itself now has 130 member companies. EV100 aims by 2030 to switch all fleet vehicles under 7.5 t to EVs and to install charging infrastructure for employees and customers. In total, EV100 members have now committed to electrify nearly 725 000 vehicles in their own fleets, and over 5 million leased vehicles.

EV100+

The EV100+ campaign was launched in 2022 by the Climate Group, the originators of the EV100 aimed at LDVs. Signatories of the EV100+ campaign commit to transition their fleet of vehicles over 7.5 t to zero-emission by 2040 in OECD markets, China and India. Founding members include a few corporate fleet owners or users.

Recent actions included setting up a broader coalition of truck makers, transport operators, shippers and retailers, energy providers and infrastructure operators and calling for ambitious targets in the (then upcoming) EU HDV CO2 regulations, such as a binding ZEV target for 2035 with only limited exceptions, and interim targets of 30% emissions reduction by 2027, and 65% by 2030. The call was also signed by CALSTART. EV100+ also signed a similar open letter by Transport & Environment, demonstrating their alignment on the issue.

References

More comprehensive policy coverage and analysis, both regionally and prior to 2022-2023, can be found online in the interactive IEA Global EV Policy Explorer. The explorer now includes policies and targets from around 90 countries, covering the majority of the annual global sales shares of LDVs (over 90%), HDVs (70%), and two/three-wheelers (almost 70%) respectively. In particular, new entries for EMDEs have been added. The explorer provides information on government policies, ambitions and targets encouraging EV adoption across all road transport segments. It covers vehicle deployment targets, financial incentives, manufacturing policies, as well as targets and financial support for charging infrastructure.

Includes battery, plug-in, and fuel cell electric vehicles.

The policy specifically refers to “Intelligent and Connected New Energy Vehicles”, and therefore may not necessarily mean 10% of total NEV sales in China.

This requirement stipulates that: 1) in 2023, 40% or more of the battery critical minerals must be extracted or processed in the United States or a US free trade country, or have been recycled in North America, gradually increasing to 80% in 2027 and beyond; and 2) in 2023, 50% of the value of the components in the battery must be manufactured or assembled in North America, gradually increasing to 100% in 2029 and beyond.

Also included in the budget is provision of “workforce development and training, and planning and technical activities”.

The total viable resource will be significantly lower than the inferred resource.

These limits apply to M1 vehicles (passenger cars with up to 8 seats). The limits for N1 vehicles (vans less than 3.5 t) are 75% and 65% respectively.

Includes passenger cars, SUVs, and pickup trucks, but not LCVs, which accounted for 6% of US LDV sales in 2022.

Between 2030 and 2035, new cars and vans can be sold if they have significant zero-emission capability, which would include some plug-in and hybrid electric vehicles. The definition of significant zero-emission capability will be consulted on later this year.

Rates for commercial applicants have reduced between 2022 and 2023.

Note by the Republic of Türkiye: The information in this document with reference to “Cyprus” relates to the southern part of the Island. There is no single authority representing both Turkish and Greek Cypriot people on the Island. Türkiye recognises the Turkish Republic of Northern Cyprus (TRNC). Until a lasting and equitable solution is found within the context of the United Nations, Türkiye shall preserve its position concerning the “Cyprus issue”. Note by all the European Union Member States of the OECD and the European Union: The Republic of Cyprus is recognised by all members of the United Nations with the exception of Türkiye. The information in this document relates to the area under the effective control of the Government of the Republic of Cyprus.

The grant was first available in 2011 and capped at 25% of the vehicle cost (to a maximum of GBP 5 000 (USD 6 170)); this was then set to GBP 4 500 (USD 5 550) in 2016, reducing between GBP 500 and GBP 1 000 (USD 620 and 1 230) per year thereafter.

This funding specifically excludes private vehicles and cannot be used to fund direct costs for LDVs.

Austria, Azerbaijan, Belgium, Cabo Verde, Canada, Chile, Croatia, Cyprus, Denmark, El Salvador, Finland, France, Greece, Iceland, Ireland, Israel, Liechtenstein, Lithuania, Luxembourg, Malta, Netherlands, New Zealand, Norway, Poland, Slovenia, Spain, Sweden, the Holy See, and the United Kingdom.

Armenia, Dominican Republic, Ghana, India, Kenya, Mexico, Morocco, Paraguay, Rwanda, Türkiye, and Ukraine.

Australia, Canada, Germany, Israel, Netherlands, New Zealand, Norway, Sweden, and the United States.

Includes leases.

Previous signatories are Austria, Canada, Chile, Denmark, Finland, Luxembourg, Netherlands, New Zealand, Norway, Portugal, Scotland, Switzerland, Türkiye, United Kingdom, Uruguay, and Wales.

Reference 1

More comprehensive policy coverage and analysis, both regionally and prior to 2022-2023, can be found online in the interactive IEA Global EV Policy Explorer. The explorer now includes policies and targets from around 90 countries, covering the majority of the annual global sales shares of LDVs (over 90%), HDVs (70%), and two/three-wheelers (almost 70%) respectively. In particular, new entries for EMDEs have been added. The explorer provides information on government policies, ambitions and targets encouraging EV adoption across all road transport segments. It covers vehicle deployment targets, financial incentives, manufacturing policies, as well as targets and financial support for charging infrastructure.

Reference 2

Includes battery, plug-in, and fuel cell electric vehicles.

Reference 3

The policy specifically refers to “Intelligent and Connected New Energy Vehicles”, and therefore may not necessarily mean 10% of total NEV sales in China.

Reference 4

This requirement stipulates that: 1) in 2023, 40% or more of the battery critical minerals must be extracted or processed in the United States or a US free trade country, or have been recycled in North America, gradually increasing to 80% in 2027 and beyond; and 2) in 2023, 50% of the value of the components in the battery must be manufactured or assembled in North America, gradually increasing to 100% in 2029 and beyond.

Reference 5

Also included in the budget is provision of “workforce development and training, and planning and technical activities”.

Reference 6

The total viable resource will be significantly lower than the inferred resource.

Reference 7

These limits apply to M1 vehicles (passenger cars with up to 8 seats). The limits for N1 vehicles (vans less than 3.5 t) are 75% and 65% respectively.

Reference 8

Includes passenger cars, SUVs, and pickup trucks, but not LCVs, which accounted for 6% of US LDV sales in 2022.

Reference 9

Between 2030 and 2035, new cars and vans can be sold if they have significant zero-emission capability, which would include some plug-in and hybrid electric vehicles. The definition of significant zero-emission capability will be consulted on later this year.

Reference 10

Rates for commercial applicants have reduced between 2022 and 2023.

Reference 11

Note by the Republic of Türkiye: The information in this document with reference to “Cyprus” relates to the southern part of the Island. There is no single authority representing both Turkish and Greek Cypriot people on the Island. Türkiye recognises the Turkish Republic of Northern Cyprus (TRNC). Until a lasting and equitable solution is found within the context of the United Nations, Türkiye shall preserve its position concerning the “Cyprus issue”. Note by all the European Union Member States of the OECD and the European Union: The Republic of Cyprus is recognised by all members of the United Nations with the exception of Türkiye. The information in this document relates to the area under the effective control of the Government of the Republic of Cyprus.

Reference 12

The grant was first available in 2011 and capped at 25% of the vehicle cost (to a maximum of GBP 5 000 (USD 6 170)); this was then set to GBP 4 500 (USD 5 550) in 2016, reducing between GBP 500 and GBP 1 000 (USD 620 and 1 230) per year thereafter.

Reference 13

This funding specifically excludes private vehicles and cannot be used to fund direct costs for LDVs.

Reference 14

Austria, Azerbaijan, Belgium, Cabo Verde, Canada, Chile, Croatia, Cyprus, Denmark, El Salvador, Finland, France, Greece, Iceland, Ireland, Israel, Liechtenstein, Lithuania, Luxembourg, Malta, Netherlands, New Zealand, Norway, Poland, Slovenia, Spain, Sweden, the Holy See, and the United Kingdom.

Reference 15

Armenia, Dominican Republic, Ghana, India, Kenya, Mexico, Morocco, Paraguay, Rwanda, Türkiye, and Ukraine.

Reference 16

Australia, Canada, Germany, Israel, Netherlands, New Zealand, Norway, Sweden, and the United States.

Reference 17

Includes leases.

Reference 18

Previous signatories are Austria, Canada, Chile, Denmark, Finland, Luxembourg, Netherlands, New Zealand, Norway, Portugal, Scotland, Switzerland, Türkiye, United Kingdom, Uruguay, and Wales.