Cite report

IEA (2024), Global EV Outlook 2024, IEA, Paris /reports/global-ev-outlook-2024, Licence: CC BY 4.0

Report options

Outlook for electric mobility

Vehicle outlook by mode

The global electric vehicle fleet is set to grow twelve-fold by 2035 under stated policies

In the STEPS, the stock of EVs across all modes except for two/three-wheelers (2/3Ws),1 grows from less than 45 million in 2023 to 250 million in 2030 and reaches 525 million in 2035. As a result, in 2035, more than one in four vehicles on the road is electric. On average, the EV stock grows by 23% annually from 2023 to 2035.

In the APS, the stock of EVs (excluding 2/3Ws) reaches 585 million in 2035, over 10% higher than in the STEPS, and 30% of the vehicle fleet (excluding 2/3Ws) is electric. Compared to the STEPS, the average annual growth in the EV fleet is only slightly higher, with an average 24% growth between 2023 and 2035. In the NZE Scenario, the fleet of EVs grows even more quickly, at an average annual rate of 27% to 2035, reaching 790 million (excluding 2/3Ws).

In the STEPS, EV sales (excluding 2/3Ws) reach almost 45 million in 2030 and close to 65 million in 2035, up from around 14 million in 2023. The sales share of EVs grows from around 15% in 2023 to almost 40% in 2030 and over 50% in 2035 in the STEPS. In the APS, the sales shares are higher, approaching 45% in 2030 and two-thirds in 2035. In the NZE Scenario, EV sales shares accelerate over the next few years, reaching about 65% in 2030 and 95% in 2035.

Electric vehicle sales by region and scenario, 2030 and 2035

OpenThe global sales shares of electric light-duty vehicles (LDVs), buses and trucks are fairly similar in both the STEPS and APS to 2030, suggesting that the gap between policy implementation and announced ambitions is small over the near term. This gap grows to 2035, given that many policies are focused on the near- to medium term, while strategy documents outlining ambitions tend to be longer-sighted.

Further, the gap between announced ambitions and a global trajectory to achieving net zero emissions by 2050 is larger than the policy implementation gap. In the NZE Scenario, 100% of light vehicle sales, including 2/3Ws, cars and vans, are zero-emission vehicles by 2035. This compares to an EV sales share of only around 75% of 2/3Ws and 70% of LDVs in the APS. Ambition for heavy-duty vehicles (HDVs), in particular, is lagging behind the net zero by 2050 pathway.

There are, however, differences by region. China, Europe and the United States, -- the largest vehicle and EV markets today – all have both ambitious targets and ambitious policies to achieve those targets. This is well illustrated by the extremely small gap between electric car sales in the STEPS and in the APS in 2030. In fact, electric car sales in 2030 in the STEPS in China, Europe and the United States together reach a sales share of over 60%, close to the global electric car sales share in the NZE Scenario. For other countries with less developed markets, the gap between projected sales in 2030 under the STEPS, APS and NZE Scenario is larger (with less than 20% electric car sales in aggregate in the STEPS and 30% in the APS), suggesting a need to both further expand the EV industry and to share policy learnings on implementation.

Global electric light-duty vehicle sales are set to reach 40% in 2030 and almost 55% in 2035 based on current policy settings

Light-duty vehicles (LDVs), including passenger light-duty vehicles (PLDVs) and light commercial vehicles (LCVs), are expected to continue to make up the majority of EVs (excluding 2/3Ws) through 2035. This is a result of strong policy support, including light-duty vehicle fuel economy and CO2 standards, as well as the availability of EV models and, more generally, the sheer size of the LDV market. For example, over the past year, Canada and the United Kingdom implemented policies to increase zero-emission vehicle (ZEV) sales in 2030, targeting 60% and 80% of PLDVs, respectively.

As a result, electric LDV sales are projected to triple to over 43 million in 2030 in the STEPS, accounting for 40% of total LDV sales. By 2035, sales reach 60 million, representing a share of almost 55%.

In this scenario, the number of internal combustion engine (ICE) cars on the roads worldwide is set to decline over time as the number of electric cars grows. The stock of electric LDVs reaches about 245 million in 2030, meaning that almost one in six LDVs on the road is electric. In 2035, electric LDV stock increases to 505 million: approximately one out of three LDVs on the road.

In the APS, sales of electric LDVs reach 47 million in 2030 and 75 million in 2035, representing two-thirds of sales in 2035. This reflects government electrification ambitions and net zero pledges, such as the Zero Emission Vehicles Declaration to achieve 100% zero-emission LDV sales by 2040, and by 2035 in leading markets, which has been signed by 40 national governments spanning six continents. The fleet of electric LDVs reaches more than 565 million in 2035, representing one in three LDVs. Of these, 525 million are electric PLDVs, with only 7% being LCVs.

China is set to remain the leading region for electric LDV sales in the STEPS, though its share in global sales is expected to shrink from almost 60% in 2023 to around 40% in 2030 and 2035. The relative decline in China’s global share is due in part to the United States nearly doubling its share of global electric LDV sales to around one-fifth in both 2030 and 2035, thanks to a combination of policy efforts and industry ramp-up (see below). Despite strong growth in electric LDV sales in the STEPS, Europe’s share of global sales remains broadly stable through 2035, at around 25%.

Full electrification of two/three-wheelers is within reach but requires more policy support

The stock of 2/3Ws is currently the most electrified among all road transport segments, with around 65 million electric 2/3Ws on the road today, representing about 8% of the fleet. In the STEPS, the number of electric 2/3Ws reaches 210 million by 2030 and 360 million in 2035, over one-third of the total fleet.

This trend has been supported by policy measures such as purchase subsidies in countries including India and Indonesia, and targets for electrifying the 2/3W fleet, predominantly in emerging and developing economies, which represent 90% of the global conventional 2/3Ws stock today. For example, the Dominican Republic aims for 5% of the private motorcycle fleet to be electric by 2030, Pakistan targets 50% electric 2/3W sales by 2030, and Rwanda targets a 30% fleet share of electric 2/3Ws. In the APS, the stock grows to 430 million in 2035, meaning 40% of all 2/3Ws on the roads are electric. The sales share of electric 2/3Ws in 2035 reaches 60% in the STEPS and 75% in the APS. China is the front-runner, with a sales share of around 90% by 2035 in both scenarios.

In the NZE Scenario, the global electric 2/3W sales share reaches close to 80% by 2030 and 100% by 2035. Getting on track with the NZE Scenario is achievable with no technological breakthroughs or major market adaptations. Given the light weight and limited daily driving distance of 2/3Ws, electrification is relatively easy and already makes economic sense on a total cost of ownership basis in many countries. However, unlike for cars, vans and HDVs, there are currently no global initiatives to reach 100% zero-emission 2/3W sales. Strengthening regulations on emissions (or even noise pollution) from 2/3Ws can play a key role in increasing the adoption of electric 2/3Ws, along with purchase subsidies to ease any barriers for lower-income households presented by higher purchase prices compared to ICE 2/3Ws.

Electric buses are projected to represent 30% of buses sold globally by 2035 based on existing policies

In recent years, a number of governments have announced new funding for electric and zero-emission buses. For example, the United Kingdom has launched a second iteration of its zero emission bus programme that will provide GBP 129 million (almost USD 160 million) to support deployment over the next few years. As announced in late 2023, India is targeting 50 000 electric buses on its roads by 2027. There are also longer-standing programmes, such as the Zero Emission Bus Rapid-deployment Accelerator partnership that was launched in 2019 to accelerate the deployment of zero-emission buses in major Latin American cities.

Funding programmes of this kind, and heavy-duty vehicles regulations, including the European Union’s revised CO2 emission standards for HDVs and California’s Advanced Clean Fleets, are expected to increase the sales shares of electric buses. In the STEPS, electric bus sales increase fourteen-fold from 2023 levels, to about half a million in 2035, representing 30% of bus sales. The stock reaches 4.5 million in 2035 in the STEPS, or 20% of the total.

There are also ambitious targets for electrifying bus fleets, including Chile (100% zero-emission vehicle sales for public transport by 2035), Colombia (100% zero-emission bus sales by 2035), Chinese Taipei (full conversion of the urban bus fleet to electric by 2030), Ecuador (100% electric new public transport vehicles by 2025), and Israel (all new municipal buses to be electric by 2025). Further, the Philippines and Solomon Islands recently joined countries including the Dominican Republic, Nepal, Pakistan and Panama in setting specific targets for decarbonising their bus fleets.2 Perhaps the biggest push for electric buses in emerging markets and developing economies (EMDEs) has been at the city level. Jakarta, Indonesia, aims to electrify its fleet of 10 000 buses by 2030, with the first 100 purchased in late 2023. Uzbekistan aims to purchase 300 electric buses in its capital Tashkent and in Samarkand. Buenos Aires is targeting a 50% zero-emission bus fleet by 2030, and a wider study of 32 Latin American cities expects that 25 000 electric buses will be deployed by 2030, and 55 000 by 2050.

Such targets mean that in the APS, sales of electric buses in 2035 are almost 40% higher than in the STEPS, reaching almost 1 million sales. One in four buses on the road in 2035 is electric. In the NZE Scenario, electric bus sales reach significantly higher levels: by 2035, almost 90% of bus sales are electric.

Trucks continue to be slowest to electrify, but country commitments could help boost progress

Zero emissions vehicles could achieve total cost of ownership parity in many HDV applications this decade, including long-haul trucks, according to recent research. And the adoption of stringent emissions standards could also help to make electric options more attractive by increasing the cost of ICE buses and trucks. Nevertheless, medium- and heavy-duty trucks may prove more difficult to electrify than other segments, in part due to the size and weight of their batteries, as well as charging requirements.

Recent emissions standards in the United States and European Union will support electric HDV adoption in the coming years. In the STEPS, sales increase more than 30-fold by 2035, albeit from around 54 000 in 2023. As a result, more than 20% of medium- and heavy-duty truck sales are electric in 2035.

At COP 28, six countries3 joined the Global Memorandum of Understanding on Zero-Emission Medium- and Heavy-Duty Vehicles (Global MOU), bringing the total to 33 nations4 committed to reaching 100% zero-emission sales in 2040 and 30% by 2030. In aggregate, these signatories currently represent almost 25% of the global medium- and heavy-duty truck market. This brings the global electric truck sales share in the APS close to 30% in 2035.

In the NZE Scenario, electric truck sales represent over 55% of total medium- and heavy-duty truck sales in 2035.

Vehicle outlook by region

China is expected to surpass a 50% electric car sales share in the next few years

The current momentum in electric car sales has led to anticipation in China that passenger new energy vehicle (NEV) sales could reach a 50% share as soon as 2025, as stated in the recent Automotive Industry Green and Low-Carbon Development Roadmap 1.0 developed under the supervision of China’s Ministry of Industry and Information Technology. If this materialises, it would be a decade ahead of the 50% sales in 2035 target laid out in the Energy-saving and New Energy Vehicle Technology Roadmap 2.0 published just a few years ago. Moreover, it would be well above the official target of 20% new energy car sales by 2025, and would even exceed the recently announced 45% NEV sales share target for 2027.

After achieving this milestone, the sales share of electric cars and vans continues to grow in the STEPS, exceeding two-thirds of total sales in 2030 and almost reaching 85% in 2035. Given that the current trend is tracking ahead of government targets, the electric LDV sales shares are the same for STEPS and APS through 2035. However, it will be critical for China to roll out public charging infrastructure in a timely manner to enable such growth. Electric LDVs are generally cost-competitive in China even at purchase, and so the phasing out of EV purchase subsidies in 2023 is unlikely to affect further growth. Announced EV battery manufacturing capacity is well above projected sales share (see below), with an eye to potential exports, and so even higher shares are theoretically achievable.

China is also the global leader in terms of electric share of the 2/3W fleet, with over one-third of all 2/3Ws being electric today, and is expected to remain the leader in electric 2/3W sales in both the STEPS and APS. In the STEPS, the sales share of electric 2/3Ws reaches nearly 90% in 2035; in the APS, the share is slightly above that by 2035.

China also has one of the highest stock shares of electric buses, with more than one in four buses being electric. By 2035, the sales share of electric buses increases to over 70% in both scenarios, up from 50% in 2023. While sales of electric medium- and heavy-duty trucks are significantly lower than other road modes, China held over 90% of the world’s total global electric truck stock in 2023. Electric truck sales are projected to reach a sales share of almost 50% in 2035 in both scenarios.

The sales share of EVs across all road transport modes (excluding 2/3Ws) reaches around 80% in 2035 in both scenarios. Across all modes, the current market dynamics, and the policy landscape as considered in the STEPS to 2035, are sufficient to bring EV sales shares into line with China’s ambition of climate neutrality by 2060, as well as with provincial electrification targets. As such, in China there is no gap between existing policy frameworks and future targets, and even more ambition is conceivable.

The European Union’s HDV CO2 standards brighten the outlook for electric heavy-duty vehicles

Europe remains one of the most advanced EV markets under stated policies. Last year, the United Kingdom passed the Vehicle Emissions Trading Schemes Order 2023, which mandates certain sales shares of zero-emission cars and vans, setting a target for annual ZEV sales shares for cars to increase from 22% in 2024 to 80% in 2030. Considering the policy landscape across Europe, including the UK ZEV mandate and the EU CO2 standards for cars and vans, the sales share of electric LDVs in Europe reaches nearly 60% in 2030 and 85% in 2035 in the STEPS. The ZEV sales share in 2035 does not reach 100% for a couple of reasons. First, in the United Kingdom, the annual ZEV targets for 2031-2035 have not yet been set out in the legislation and thus the 100% ZEV sales target for 2035 is not reflected in the STEPS. Secondly, the European car market includes national markets that are not covered by such strong regulations as in the European Union and the United Kingdom.

Given that the European Union has legislated to the level of its climate and EV ambitions (resulting in zero-emission LDV sales reaching 100% in 2035), and since the United Kingdom has also passed legislation for zero-emission LDVs, at least through 2030, the EV sales shares in the APS are similar to in the STEPS. Electric LDVs represent over 60% of sales in 2030 and over 90% of sales in 2035 in the APS.

For buses and trucks, the revised EU HDV CO2 standards drive up electric HDV sales in the STEPS. The standards will require 100% of city bus sales to be zero-emission from 2035, and other HDVs to reduce CO2 emissions by at least 45% in 2030, 65% in 2035 and 90% from 2040, compared to 2019 levels. A number of European countries also offer grants and other financial support for the purchase of electric buses and trucks. For example, the second round of Zero Emission Bus Regional Areas (ZEBRA) funding in the United Kingdom is expected to add an additional 955 zero-emission buses to the UK fleet. In the STEPS, the sales shares of electric buses and trucks reach around 65% and 35% in 2035 in Europe. Within the European Union, sales are higher, reaching shares of 80% for buses and around 50% for trucks in 2035.

The APS takes into account the ambitions of the 18 European national governments who have signed the Global MOU on Zero-Emission Medium- and Heavy-Duty Vehicles, committing to reach 30% zero-emission HDV sales shares in 2030 and 100% in 2040. Other targets are also included in the APS, such as the UK aim to phase out the sale of any heavy goods vehicles weighing 26 tonnes and under that are not zero emissions by 2035. As a result, in Europe in the APS, electric bus sales reach around 80% in 2035 and electric truck sales almost 45%.

In Europe, the EV sales share across all modes (excluding 2/3Ws) is 85% in 2035 in the STEPS. In the APS, Europe has a combined EV sales share of over 90% in 2035 (for electric LDVs, buses and trucks), which is in line with the global trajectory in the NZE Scenario.

In the United States, new emissions standards will boost electric car and truck sales

Electric car sales are expected to continue growing in the United States, thanks to successive policies that are driving up adoption. The Corporate Average Fuel Economy Standards for Model Years 2024-2026 Passenger Cars and Light Trucks requires fuel economy improvements that are likely to increase the share of EV sales in just the next few years. From 2026, California’s Advanced Clean Cars II regulations, which have been adopted by twelve other states and Washington DC, will begin to further increase zero-emission PLDV sales, with the stated aim of reaching 100% by 2035. Combined, these states represent around one-third of light-duty vehicle sales in the United States, with a significant impact on overall electric car sales and, therefore, on OEM strategy. This could create a ripple effect across the wider market, as OEMs harmonise around the regulations in order to bring down production costs through standardisation. In addition, in March 2024, the US Environmental Protection Agency (EPA) also released the final rulemaking for Multi-Pollutant Emissions Standards for Model Years 2027 and Later Light-Duty and Medium-Duty Vehicles, which it estimates could bring electric PLDV sales to around 70% of total sales in 2032.

The United States is also supporting an expansion of charging infrastructure to support increased EV adoption. At the end of 2023, construction of the first EV chargers funded under the National Electric Vehicle Infrastructure programme had begun, with around USD 100 million already awarded to projects. There is now around USD 2.5 billion available to states to be allocated to EV charging projects (about 60% of the total programme funding).

The policy landscape in the United States, combined with already-committed industry investments (see below), is boosting confidence in EV market expansion. As a result, electric LDV sales reach approximately 55% in 2030 in the STEPS, higher than the Administration’s previously announced target, and hit more than 70% in 2035. Due to the recent policy developments, the electric LDV sales in the STEPS match government ambition and thus are the same as in the APS.

Funded by the Bipartisan Infrastructure Law, the US EPA has awarded almost USD 2 billion to fund approximately 5 000 school bus replacements, with another USD 3 billion to be provided to 2026, as part of the Clean School Bus Program. Under stated policies, the US electric bus sales share is expected to increase from around 1% in 2023 to 35% in 2030 and 60% in 2035. With respect to trucks, 11 states, representing around one-quarter of HDV sales in the country, have adopted California’s Advanced Clean Trucks regulation, which sets ZEV sales requirements for trucks that range from 40-75% in 2035. Bringing the national standards more in line with the Californian regulation, the US EPA finalised GHG standards for HDVs for model years 2028-2032, which aims to reduce emissions from trucks and heavy buses by 25-60% in 2032 compared to 2026. In the STEPS, the electric truck sales share across the United States reaches around 50% in 2035.

The United States is also a signatory of the Global MOU, which targets 30% zero-emission M/HDV sales shares by 2030 (on aggregate, across bus and truck sales) and 100% by 2040. In the APS, the US electric bus sales share reaches around 75% in 2035 and the electric truck sales share reaches almost 70% in 2035.

The EV sales share across all modes (excluding 2/3Ws) reaches more than 70% in both the STEPS and the APS in 2035.

Japan’s policies in support of electric vehicles remain unchanged

Japan has fuel economy standards for both light- and heavy-duty vehicles, and offers purchase subsidies for EVs. Historically, Japan has also had a relatively high sales share of hybrid (non-plug-in) vehicles, as one way to reduce emissions from cars and improve the average fuel economy.

In the STEPS, the electric LDV sales share increases from about 3% in 2023 to around 20% in 2030, and 30% in 2035. In Japan’s Green Growth Strategy, the government sets a target for 100% of new car sales to be electrified by 2035 – for which their definition includes BEVs, PHEV, FCEV and hybrid electric vehicles (HEVs). In the APS, which reflects this target, about 70% of LDV sales in 2035 are electric (BEV or PHEV).

With respect to HDVs, electric bus sales reach about 25% in 2030 and increase to 50% in 2035 in the STEPS. In the APS, electric bus sales increase to 75% in 2035 to support climate targets. However, electric medium- and heavy-duty truck sales lag behind, approaching 20% in 2035 in the STEPS and about 30% in the APS.

In Japan, the EV sales share across all modes (excluding 2/3Ws) is 30% in 2035 in the STEPS and about 70% in the APS.

In India, the outlook for electric car sales brightens as domestic supply chains are built

India’s Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) II scheme, which provided subsidies for EVs and funding for EV charging, ended on 31 March 2024. The Ministry of Heavy Industries announced in March 2024 a limited scheme for the period between 1 April 2024 and 31 July 2024, which outlays over INR 4.9 billion (Indian rupees) (almost USD 60 million) to subsidise electric 2/3W purchases. This may be a stopgap until the announcement of a FAME III scheme, which is expected to detail new subsidy provisions for EVs. In addition, the government’s Production Linked Incentive scheme for Automobile and Auto Components and for manufacturing of Advanced Chemistry Cell Battery Storage aims to attract investments in domestic EV and battery manufacturing.

Based on the current policy landscape, electric LDVs represent one in four LDVs sold in India in 2035. The APS takes into account that India signed the COP 26 declaration to transition to 100% zero-emission LDV sales by 2040. As such, electric LDV sales in 2035 reach over 60% in the APS.

India has the largest stock of two-wheelers of any country and represents almost 30% of the global stock of three-wheelers. Electrifying the 2/3W segment will therefore be important for decarbonising India’s road transport system. India has made good progress to date, and almost a quarter of the country’s three-wheelers are electric. The sales share of electric 2/3Ws increases from around 8% in 2023 to almost 60% in 2035 in the STEPS. In the APS the electric sales share reaches 70% in 2035.

As announced at COP 28, India is aiming to reach a stock of 50 000 electric buses by 2027, backed by a USD 390 million fund supported by both the Indian and US governments to provide loans to expand electric bus manufacturing. In both the STEPS and the APS, electric bus sales shares increase to about 35% in 2030 and 60% in 2035. Electric truck sales remain low in both scenarios to 2035, at under 10%.

Across all modes (including 2/3Ws), the EV sales share in India is about 50% in 2035 in the STEPS (and closer to 25% if 2/3Ws are excluded). In the APS, EV sales shares in India scale up to over 65% in 2035 across all road vehicle modes (and to almost 60% excluding 2/3Ws).

Many emerging and developing economies set their sights on electrification of two- and three-wheelers and public transport

Each year, more and more countries around the world are setting out a clear vision or targets for electromobility. However, in emerging and developing economies, in particular, adoption of EVs can be hindered by limited funding available for fiscal incentives and other measures to overcome purchase price hurdles. Importantly, there are still some 750 million people without access to electricity, mainly in sub-Saharan Africa, and others with grid reliability issues, which also affects the prospects for charging EVs. However, efforts are being made to support governments in EMDEs to advance deployment of EVs, such as through the Global Electric Mobility Programme, as well as proposed reforms that could improve financing options from Multilateral Development Banks.

In many EMDEs, the main targets of vehicle electrification initiatives are 2/3Ws and public transport. In Colombia, for example, there has been a major focus on electrifying mass transportation systems (buses), cargo vehicles and taxis. Targets for electric 2/3Ws have been set in countries as diverse as Cambodia, Morocco and the Dominican Republic.

In the STEPS, the average EV sales share across regions and countries outside of those described in the preceding sections is about 45% for 2/3Ws, 20% for buses, 18% for LDVs and 3% for trucks in 2035. In the APS, sales across these other regions reach 65% of 2/3Ws, 40% of LDVs, 30% of buses and 10% of trucks.

The countries that have adopted EV-related policies and set ambitions tend to have higher EV sales shares than these averages. In particular, Canada tends to align with the most ambitious standards in North America. In December 2023, Canada amended its GHG regulations to include new requirements to increase the availability of zero-emission passenger cars and light trucks, targeting at least 20% zero-emission vehicle sales by 2026, at least 60% by 2030 and 100% zero-emission vehicle sales by 2035.

The industry outlook

The ten largest carmakers are set to sell over 20 million electric cars in 2030, exceeding current policy targets

As of 2023, the ten largest global automakers all have established clear electrification targets. Together, these automakers sold over 40 million cars in 2023, representing about 55% of global sales. Although some manufacturers have missed or postponed near-term targets – often pointing to underwhelming consumer demand – they have not scaled back their longer-term ambitions. If each company in the top ten meets their target, over 20 million new electric cars could be sold in 2030. Notable examples include BMW’s target of 50% of deliveries in 2030 to be BEVs; Toyota’s 3.5 million BEV sales target in 2030; Stellantis’s 5 million BEV sales target in 2030; and GM’s target of a global EV manufacturing capacity of 2 million per year by 2025. In addition, Tesla is targeting production of 20 million electric cars in 2030, which – combined with the targets of the top ten – would be roughly equivalent to the projected sales in the STEPS in that year.

In total, more than 20 OEMs, together representing over 90% of car sales in 2023, have set some sort of target for future EV deployment. The global electric car sales envisaged in announcements by manufacturers have increased by several percentage points based on developments over the past year. If all manufacturers’ targets on vehicle electrification are combined, between 42% and 58% of car sales in 2030 could be electric. This range encompasses the sales share for cars in the STEPS (almost 45%) and the share implied by government ambitions in the APS (almost 50%).

Regional examples include:

- In China, major carmakers, including incumbents, have increased their electrification ambitions. For example, SAIC and Geely are targeting 50% NEV sales by 2025.

- In Europe, more ambitious targets announced by majors such as Volkswagen, Ampere (a spin-out of Renault), Nissan and Suzuki have increased the overall OEM electrification targets relative to last year’s range. For example, Volkswagen increased its BEV delivery target from 70% to 80% by 2030. On the other hand, Mercedes-Benz has delayed its goal of 50% electrified car sales by 5 years, to 2030.

- In the United States, both Ford and GM missed their 2023 targets or abandoned those for 2024, citing profitability concerns, though they are maintaining longer-term targets. Ford missed its targeted manufacturing rate of 600 000 EVs per year in 2023, but now aims to achieve that in 2024. GM had previously planned to manufacture 400 000 electric cars in North America by mid-2024, but has now dropped that target, and yet has retained a US manufacturing capacity target of 1 million electric cars by 2025. Meanwhile, Volkswagen increased their BEV delivery target in the United States from 50% to 55% by 2030. As a result of missed near-term targets but robust longer-term ambition, the outlook for the United States based on OEM targets has remained stable over the past year.

- In Japan too, new announcements have increased the aggregate OEM target range. Suzuki aims to reach 20% BEV sales in 2030. Subaru announced a new and more ambitious target of 50% BEV sales out of a total of 1.2 million car sales in 2030, with a production capacity of 400 000 BEVs in Japan and even a new BEV production line in the United States before 2030. Subaru plans to introduce a total of 8 new BEV models, and to sell 400 000 BEVs in the United States by 2028.

- In India, Tata is targeting a 50% EV sales share by 2030 and net zero GHG emissions by 2045.

Newly announced and updated electrification targets for light-duty vehicles

|

Automaker |

Target |

Region |

Group / Brand |

|---|---|---|---|

|

Increased BEV delivery target from 50% to 55% in 2030 |

United States |

Brand |

|

|

Increased BEV delivery target from 70% to 80% in 2030 |

Europe |

Brand |

|

|

Announced target of 300 000 BEV sales in 2025 and 1 million in 2031 |

Europe |

Brand |

|

|

Targets delivery of 1 million electric cars by 2030 |

Europe |

Brand |

|

|

Accelerated production target to 20% EV by 2026 |

Europe |

Brand |

|

|

Announced 100% BEV sales from 2030 |

Europe |

Group |

|

|

Presented strategy to reach 80% BEV sales share in 2030 |

Europe |

Group |

|

|

Presented strategy to reach 15% BEV sales share in 2030 |

India |

Group |

|

|

Presented strategy to reach 20% BEV sales share in 2030 |

Japan |

Group |

|

|

Announced more ambitious target of 50% BEV sales in 2030 |

Global |

Group |

|

|

Raised ambition to sell 2 million EVs annually by 2030 |

Global |

Brand |

|

|

Increased 2030 EV sales target to 1.6 million |

Global |

Brand |

|

|

Announced plan to sell 50% EVs by 2030 |

Global |

Brand |

|

|

Increased ambition from 40% to 50% ZEV sales by 2025 |

Global |

Group |

|

|

Increased ambition from 40% to 50% ZEV sales by 2025 |

Global |

Group |

Data on targets announced or updated since the publication of GEVO-2023. Source: IEA analysis based on company announcements as linked in the automaker column.

Several important car makers have also announced a phase-out date for ICE vehicle sales. For example, ICE phase-outs have been announced by Jaguar from 2025, Mini and Rolls-Royce from the beginning of the 2030s, Lexus from 2035, Land Rover from 2036, and Honda from 2040.6 Combined, these brands represented over 5% of global car sales in 2023. Even more automakers have pledged to phase out ICE vehicle sales in the European market specifically, including include Ford, Volkswagen, Stellantis, Lancia, Renault and Nissan.

Policy is boosting investment in manufacturing capacity, building confidence for a rapid electrification pathway

Battery and EV manufacturers have faced new challenges and opportunities as major markets including the United States and the European Union introduced new industrial policies. Domestic content requirements introduced by these policies have supported the expansion plans of major battery and EV manufacturers, with billions in investments already committed as of early 2024. Worldwide, reported investment announcements from 2022 and 2023 alone exceed USD 275 billion in EVs and USD 195 billion in batteries, with around USD 190 billion of the total already committed. The level of investments observed in the past 2 years boosts confidence in the electrification of road transport.

In China, committed battery manufacturing capacity is well above what is needed to supply domestic electric car sales in 2030. In fact, just two-thirds of the already-committed battery cell manufacturing capacity would be sufficient to cover 100% of electric car sales in China in 2030. This excess capacity, which is today driving down margins, implies that battery producers are banking on export markets, at least in part. This will bring both opportunities and challenges. Countries that have electrification targets but lack sufficient battery manufacturing capacity could reach these targets through imports from China, whereas companies outside of China will see increased competition from the arrival of Chinese manufacturers. Governments will seek to find the right balance between supporting local producers at the same time as ensuring consumers can benefit from the low prices offered by Chinese manufacturers, which would accelerate road electrification.

In the United States, the Inflation Reduction Act (IRA) revised the requirements for the Clean Vehicle Tax Credit. Now, to qualify for the tax credit of up to USD 7 500, vehicle assembly must take place in North America and meet the critical minerals and battery components requirements.7 In December 2023, guidance was released defining the "Foreign Entities of Concern” as part of the tax credit exclusions: vehicles with batteries containing components manufactured or assembled by a foreign entity of concern (which includes China) cannot qualify for the tax credit. The number of eligible electric car models has therefore fallen from more than 40 in the second half of 2023 to around 27 from the beginning of January 2024.8 In 2025, restrictions may be expanded such that EVs cannot qualify if their batteries contain any critical minerals that were extracted, processed, or recycled by a foreign entity of concern.

From September 2022 to the end of 2023, after the IRA was signed into law, investments of more than USD 60 billion were announced to support the EV industry, in EV manufacturing, charging and batteries in the United States.9 The vast majority – about 80% – of these investments are for batteries; with just around USD 5 billion announced for EVs, though there are, of course, strong links between battery manufacturing and EV manufacturing. For example, in February 2024, Volkswagen-backed Scout Motors started building a USD 2 billion electric sports utility vehicle (SUV) manufacturing plant in South Carolina. In mid-2023, BMW broke ground on their high-voltage battery manufacturing plant (USD 700 million) to supply batteries for their announced EV production lines (USD 1 billion) in South Carolina. Hyundai-Kia, which in 2023 overtook GM and Ford in terms of electric car sales share, plans to manufacture EVs in the state of Georgia by October 2024 to qualify for IRA benefits.

Announced battery manufacturing expansions in the United States, in part resulting from signals sent by the IRA, would be more than enough to satisfy carmaker electrification targets and government ambitions in 2030. Of course, the announced investments in battery manufacturing will first need to be realised, and we estimate that it would require around USD 100 billion in capital expenditures10 to reach the level of battery manufacturing capacity necessary to meet demand for electric cars in 2030 in the APS. According to the Clean Investment Monitor, actual expenditures in EV battery manufacturing from 2020 to 2023 totalled around USD 45 billion. Around 45% of the capital expenditure (CAPEX) needed for battery manufacturing has therefore already been spent.

In the European Union, the Net Zero Industry Act and the subsequent relaxing of state aid rules in March 2023 are boosting public support for road transport electrification. For example, in January 2024, Swedish battery maker Northvolt received approval for EUR 700 million in direct grant and EUR 200 million in guarantee from Germany, which was described as “proportionate and limited to the minimum necessary to trigger the investment in Europe”. Northvolt’s project is expected to require a total investment of EUR 4.5 billion, creating 3 000 jobs and starting battery manufacturing in 2026. The company also secured a USD 5 billion green loan – touted as the largest green loan in Europe to date – with the support of European and Korean banks and export credit agencies. The loan will enable further expansion for the production of cathodes, cell manufacturing and a recycling plant in northern Sweden.

As of 2024, the market signals provided by the Net Zero Industry Act have been sufficient to attract enough committed investments in battery manufacturing capacity in the European Union to satisfy government electrification targets out to 2030. Across the whole of Europe, committed investments come close to meeting these targets.

While investments that are already committed today tend to be more heavily geared towards battery than to EV manufacturing, it is important to note that battery manufacturing and EV expansion plans typically go hand in hand, often being situated close to demand centres to create integrated supply chains. This close collaboration is important in order to deliver on targets, avoid bottlenecks and decrease costs. In addition, in the event that committed EV battery manufacturing capacity outpaces demand from EV manufacturers, it is unlikely that it would find alternative outlets, as other key battery markets such as consumer electronics are already well supplied and have different technical specifications. Failure to deliver on EV manufacturing capacity and sales therefore creates a risk of massive sunk investment in battery manufacturing, if manufacturers are unable to export significant quantities.

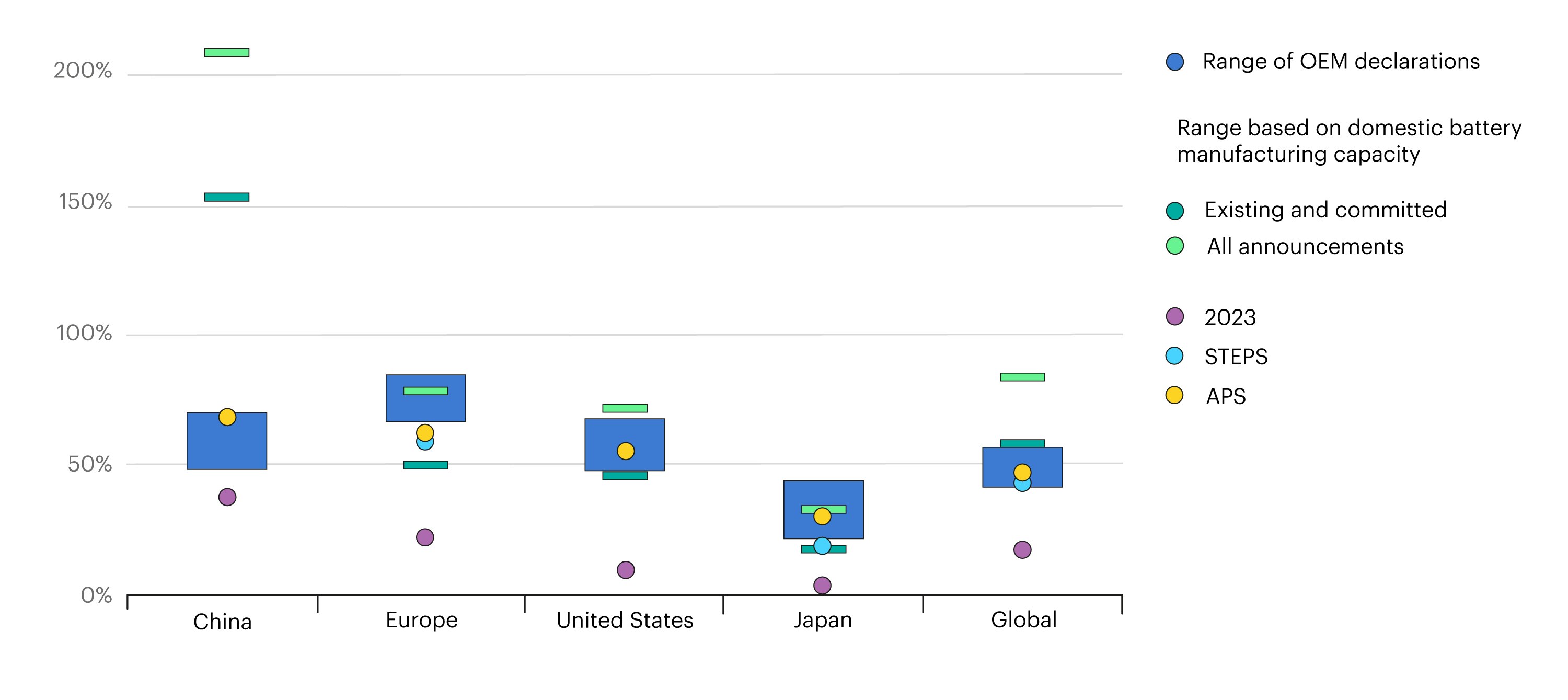

Equivalent electric car sales shares targets by battery and car manufacturers, and electric car sales shares in the Stated Policies and Announced Pledges Scenarios, 2030

Open

{kind=link}

For example, in Europe, Volkswagen benefits from close co-operation with two of the biggest regional battery manufacturers, LG Energy Solutions and Samsung, which together provide batteries for 95% of Volkswagen’s European electric car sales. In China, on the other hand, Volkswagen works with CATL, which provides almost all the batteries for its Chinese electric car sales. Similarly, Tesla works with Panasonic’s Nevada plant in the United States, but with CATL and LG Energy Solutions in China. When considering expansion plans, battery manufacturers often seek to bring operations closer to the production facilities of partner OEMs. CATL is currently developing manufacturing facilities in Hungary to provide regional car makers like Stellantis, which sources nearly 50% of its European EV batteries from CATL and the other half from LG and Samsung SDI. A similar trend is already observable outside of the biggest EV markets, such as in Türkiye, where the Turkish brand Togg and Farasis Energy created a joint venture in April 2023. During 2023 the Togg T10X model reached almost 20 000 registrations in Türkiye, becoming the fourth most sold car model in November 2023.

Continued co-operation between EV and battery makers is expected to continue to support road transport electrification into the future. As of early 2024, half of the committed battery manufacturing capacity in the United States will be delivered by joint ventures between an EV and a battery manufacturer (e.g. LG-GM, LG-Honda, LG-Hyundai, Samsung-GM, Samsung-Stellantis, Panasonic-Tesla, LG-Toyota, SKI-Ford, SKI-Hyundai). Many similar joint ventures are seen in Europe (e.g. Northvolt-Volvo, Envision-Nissan). There are even joint ventures for battery components, such as between Volkswagen and Umicore to produce battery cathodes.

Globally, on the basis of industry announcements, committed battery manufacturing capacity in 2030 would be sufficient to support the electric car sales share reaching more than 55%, higher than the sales shares implied by automaker targets and both the STEPS and APS projections. In fact, the committed and existing battery manufacturing capacity would meet over 90% of the EV battery demand in the NZE Scenario in 2030.

Heavy-duty original equipment manufacturers are most ambitious in the European market, driven by proposed CO2 standards

A few new announcements on zero-emission vehicle strategies have been seen in the HDV market, such as the agreement signed by Hino Motors Sales USA that could result in the delivery of up to 10 000 electric trucks by 2030. For the United States, the range of OEM targets in 2030 encompasses the zero-emission vehicle sales shares in the STEPS (around 20%).

Chinese OEM Foton has also announced a target of 50% NEV sales by 2030. Similarly, BAIC Trucks also plans to sell 50% new energy trucks by 2030 and 80% by 2035. On aggregate, OEM targets would imply that zero-emission truck sales represent 13-32% of Chinese truck sales in 2030.

There have been no big announcements from truck makers in Europe over the past year, but OEM targets for this market still exceed what would be necessary under the EU HDV CO2 standard, as reflected in the STEPS sales share.

References

In this report, “two/three-wheelers” refer to vehicles aligned with the following UNECE classifications: L1, L2, L3, L4 and L5.

See the Global EV Policy Explorer for a more comprehensive list of countries and policies.

New signatories were Cape Verde, Colombia, Ghana, Iceland, Israel and Papua New Guinea.

Previous signatories comprise Aruba, Austria, Belgium, Canada, Chile, Croatia, Curaçao, Denmark, Dominican Republic, Finland, Ireland, Liechtenstein, Lithuania, Luxembourg, Netherlands, New Zealand, Norway, Portugal, Scotland, Sint Maarten, Switzerland, Türkiye, Ukraine, United Kingdom, United States, Uruguay and Wales.

The California Air Resources Board has requested a waiver from the US Environmental Protection Agency for the regulation to be enforceable; a waiver has not yet been granted. Given that such a waiver was granted for the previous Advanced Clean Cars regulation, this regulation is included in the STEPS. Note also that three states have only partially adopted the Advanced Clean Cars II regulation, keeping the ZEV sales shares targets only through 2032 without including the 100% sales target for 2035.

Mercedez-Benz had previously announced the end of ICE car sales this decade but has recently delayed that target.

The critical minerals requirement refers to minimum percentages of critical mineral extraction or processing (by values) in the United States or in a country which has a free trade agreement with the United States. The battery component requirement refers to minimum percentages of battery component manufacturing or assembly (by value) that takes place in North America.

Based on model trim eligibility from the US government website.

Another USD 5 billion has been invested in battery manufacturing in Canada since the IRA was passed.

CAPEX of 2023 USD 107 million per GWh of battery manufacturing capacity is assumed.

Reference 1

In this report, “two/three-wheelers” refer to vehicles aligned with the following UNECE classifications: L1, L2, L3, L4 and L5.

Reference 2

See the Global EV Policy Explorer for a more comprehensive list of countries and policies.

Reference 3

New signatories were Cape Verde, Colombia, Ghana, Iceland, Israel and Papua New Guinea.

Reference 4

Previous signatories comprise Aruba, Austria, Belgium, Canada, Chile, Croatia, Curaçao, Denmark, Dominican Republic, Finland, Ireland, Liechtenstein, Lithuania, Luxembourg, Netherlands, New Zealand, Norway, Portugal, Scotland, Sint Maarten, Switzerland, Türkiye, Ukraine, United Kingdom, United States, Uruguay and Wales.

Reference 5

The California Air Resources Board has requested a waiver from the US Environmental Protection Agency for the regulation to be enforceable; a waiver has not yet been granted. Given that such a waiver was granted for the previous Advanced Clean Cars regulation, this regulation is included in the STEPS. Note also that three states have only partially adopted the Advanced Clean Cars II regulation, keeping the ZEV sales shares targets only through 2032 without including the 100% sales target for 2035.

Reference 6

Mercedez-Benz had previously announced the end of ICE car sales this decade but has recently delayed that target.

Reference 7

The critical minerals requirement refers to minimum percentages of critical mineral extraction or processing (by values) in the United States or in a country which has a free trade agreement with the United States. The battery component requirement refers to minimum percentages of battery component manufacturing or assembly (by value) that takes place in North America.

Reference 8

Based on model trim eligibility from the US government website.

Reference 9

Another USD 5 billion has been invested in battery manufacturing in Canada since the IRA was passed.

Reference 10

CAPEX of 2023 USD 107 million per GWh of battery manufacturing capacity is assumed.