Cite report

IEA (2024), Global Methane Tracker 2024, IEA, Paris /reports/global-methane-tracker-2024, Licence: CC BY 4.0

What did COP28 mean for methane?

A number of new announcements to reduce methane were made at COP28 climate summit in Dubai. The outcome text from the first Global Stocktake recognises the need to substantially reduce methane emissions by 2030. The Oil and Gas Decarbonisation Charter (ODGC) was established, new countries joined the Global Methane Pledge, and new financing was mobilised to support the reduction of methane and other non-CO2 greenhouse gases (GHGs).

We estimate that if all COP28 commitments were to be achieved in full and on time, and new financing is deployed effectively, annual methane emissions would decline by nearly 25 Mt by 2030 – most of which would be reductions in emissions from oil and gas operations. Fossil fuel companies and governments around the world now need to deliver clear strategies for how they will implement these pledges effectively and rapidly. This needs to be accompanied by verification and accountability mechanisms to ensure that actors are taking the necessary steps towards their goals. Further commitments – particularly in financing – are needed to deliver the reductions required this decade.

The new Oil and Gas Decarbonisation Charter could cut emissions by nearly 20 Mt

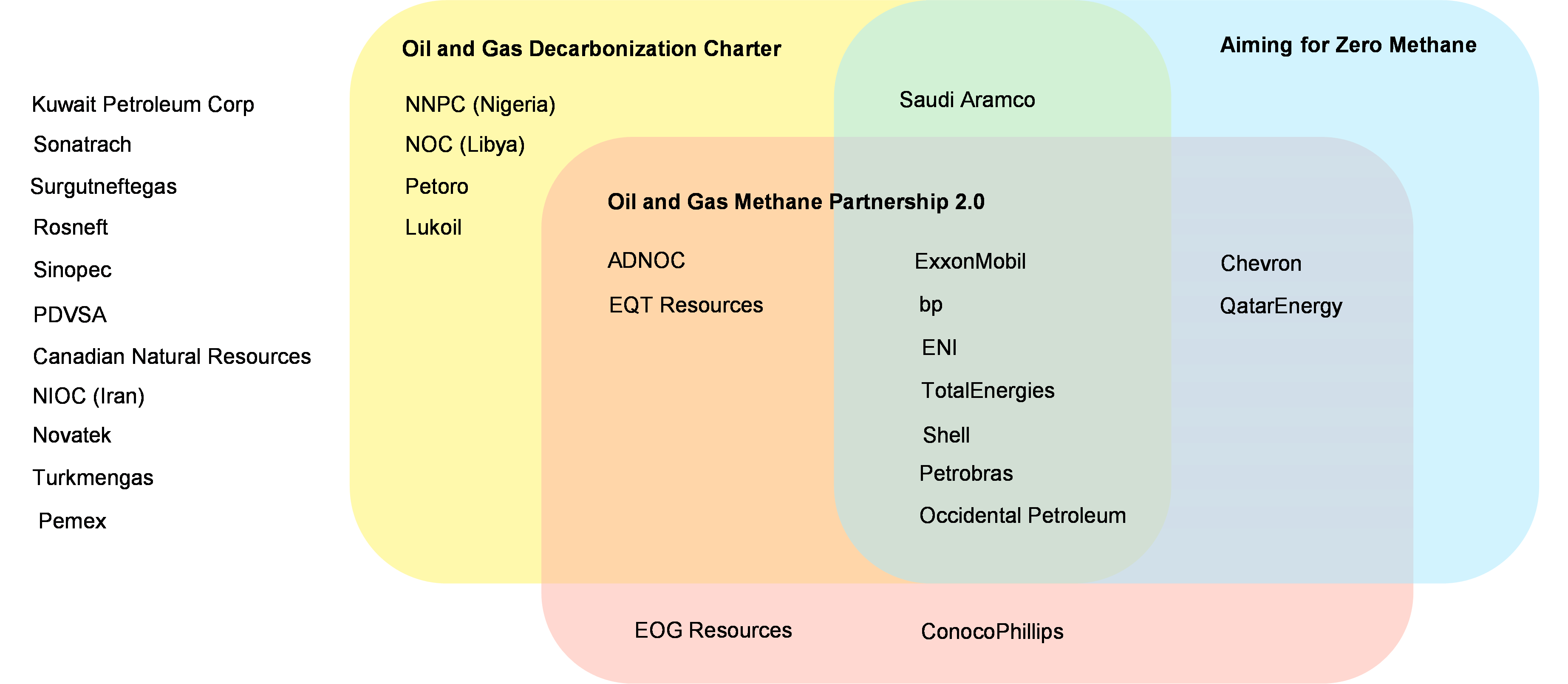

The Oil and Gas Decarbonization Charter (ODGC) launched at COP28 is an industry initiative focussed on climate action across the oil and gas sector. A total of 52 companies have joined and they aim to achieve net zero scope 1 and 2 greenhouse gas emissions from their operations by 2050 at the latest, to end routine flaring by 2030, and to achieve near-zero upstream methane emissions by 2030.

Around 30 of the companies that have joined the OGDC had not previously engaged other international initiatives to tackle methane and flaring, such as the Aiming for Zero Methane Initiative or the Oil & Gas Methane Partnership 2.0. This includes a number of National Oil Companies (NOCs), which comprise around 60% of the total number of companies that have joined the OGDC.

Signatory companies to selected international methane initiatives

Open

{kind=link}

Companies in the OGDC aim to reduce the methane intensity of their oil and gas production to 0.2% by 2030. This measure is defined as the volume of methane released from all upstream oil and gas operations divided by total volume of gas marketed. The same method is used by intensities reported by the Oil and Gas Climate Initiative (OGCI). There is a risk that this approach could complicate the comparison of methane intensities of oil-focussed operators, which could appear to have a very high intensity if marketed gas volumes are very small, and gas-focussed operators. Methane intensities reported by the IEA are based on total methane emissions from oil and natural gas supply divided by total oil and gas production, assuming methane has an energy density of 55 megajoules per kilogramme.

We estimate that the companies that have signed the OGDC are responsible for approximately one quarter of global oil and gas methane emissions. Taking into account production levels in the IEA’s Stated Policies Scenario, if these companies were all to achieve the 0.2% upstream target at operated assets, methane emissions globally would be reduced by just under 20 Mt by 2030.

The OGDC includes an aim for companies to measure, monitor, publicly report and independently verify their GHG emissions. This will be critical to the success of the OGDC and will boost public confidence in abatement efforts. One option would be to join existing reporting initiatives, such as the UN Environment Programme’s Oil & Gas Methane Partnership 2.0 (OGMP 2.0), and progress towards measurement-based estimates of emissions. Currently, 17 of the 52 OGDC companies are part of OGMP 2.0.

The methane reduction targets in the OGDC cover emissions only from operated assets, but the charter also contains an aim for companies to engage with joint operating partners to promote similar levels of performance. Doing so would significantly expand the reach of the emissions reductions.

The OGDC only addresses methane emissions from upstream operations. While upstream oil and gas operations account for around 90% of global oil and gas methane emissions, action to reduce emissions from downstream segments is also essential to keep 1.5 °C within reach.

The Global Methane Pledge continues to gain momentum

At COP28, Angola, Kazakhstan, Kenya, Romania and Turkmenistan joined the Global Methane Pledge (GMP). By joining the Pledge, countries commit to work together to collectively reduce methane emissions by at least 30% below 2020 levels by 2030. In addition, Canada, the Federated States of Micronesia, Germany, Japan and Nigeria joined the European Union and the United States in leading the GMP as “Champions,” meaning they commit to supporting progress by other GMP countries and partners while advancing progress domestically. Azerbaijan joined the GMP in March 2024, meaning there are now 156 participant countries that accounted for around 55% of global energy sector methane emissions in 2023.

The five new countries that joined the GMP at COP28 were responsible for close to 10% of fossil fuel methane emissions in 2023. We estimate that if they took full advantage of the methane abatement potential in their energy sectors, this would reduce global methane emissions by around 5 Mt by 2030.

Countries and regions that have joined the Global Methane Pledge, the Zero Routine Flaring Initiative and have methane action plans

Open

{kind=link}

A number of GMP countries announced new policy developments in the weeks leading up to COP28, during the summit, and immediately afterwards, including Canada, the European Union and the United States. Many countries also announced early-stage plans to develop or update policies and regulations to bring down methane emissions. By the end of 2023, nearly 60 governments had completed or were in the process of completing national methane action plans, with many more engaged on methane action planning.

These plans vary in their level of detail, with some detailing specific actions and timelines. For example, Brazil and Egypt both announced that they would develop regulations over the course of 2024 and 2025 with the aim to reduce methane emissions from the oil and gas sector. Kazakhstan issued a joint statement with the United States, indicating they would develop national standards to eliminate non-emergency venting and mandate leak detection and repair (LDAR) “as soon as possible and before 2030.”

Although not part of the Global Methane Pledge, China also released a national methane action plan in the lead-up to COP28, committing to enhance emissions monitoring, improve methane utilisation, and improve policy frameworks to reduce emissions. The plan does not specify methane reduction targets, but it indicates China will include measures to tackle methane emissions in its next Nationally Determined Contribution (NDC) under the Paris Agreement.

There is also an increasing trend of subnational governments looking to take action on methane within their jurisdictions. The US state of California launched a new Subnational Methane Action Coalition with signatories from fifteen subnational governments around the world to facilitate greater cooperation and the sharing of best practices.

New finance commitments will speed up action

Financing for methane abatement reached USD 14 billion in 2021/22, an 18% increase from 2019/20. Funding focussed mainly on achieving reductions in the agriculture, land use and waste, with fossil fuel methane abatement receiving less than 1% of tracked finance. Nonetheless, a number of new financing initiatives were launched during 2023 and at COP 28 that will be used to cut methane from the fossil fuel sector.

- The Methane Finance Sprint, which was launched in April 2023 by the United States with the aim of raising at least USD 200 million in new grant funding. At COP28, it was announced that more than USD 1 billion in new funding had been earmarked for methane mitigation since COP27. Governments and the European Commission contributed around USD 410 million to the Sprint, including USD 190 million from the European Commission, and the private sector contributed USD 640 million. This funding is across all sectors with a focus on reductions in low- and middle-income countries.

- The World Bank Global Flaring and Methane Reduction Partnership, which was launched at COP28 with USD 255 million in funding for oil and gas methane and flaring reduction in developing countries. This Partnership is a multi-donor trust fund comprised of governments, oil companies and multilateral organisations. Access to project development and financing support is subject to commitments on transparency and a programmatic approach to emissions reductions by 2030.

- The Global Methane Hub, which in collaboration with UNEP’s International Methane Emissions Observatory and its partners, announced USD 10 million in seed funding for a campaign to deliver increased funding to governments, businesses and others to improve data and reduce methane emissions, with a goal to reach USD 300 million in funding by COP29.

These new initiatives suggest that external sources of finance for methane cuts in the fossil fuel industry are growing, but remain below USD 1 billion. While this represents less than 1% of the spending needed from now to 2030, it should mobilise much greater levels of financing and broader support for cutting methane emissions.