Cite report

IEA, IRENA & UN Climate Change High-Level Champions (2023), Breakthrough Agenda Report 2023, IEA, Paris /reports/breakthrough-agenda-report-2023, Licence: CC BY 4.0

Report options

State of transition

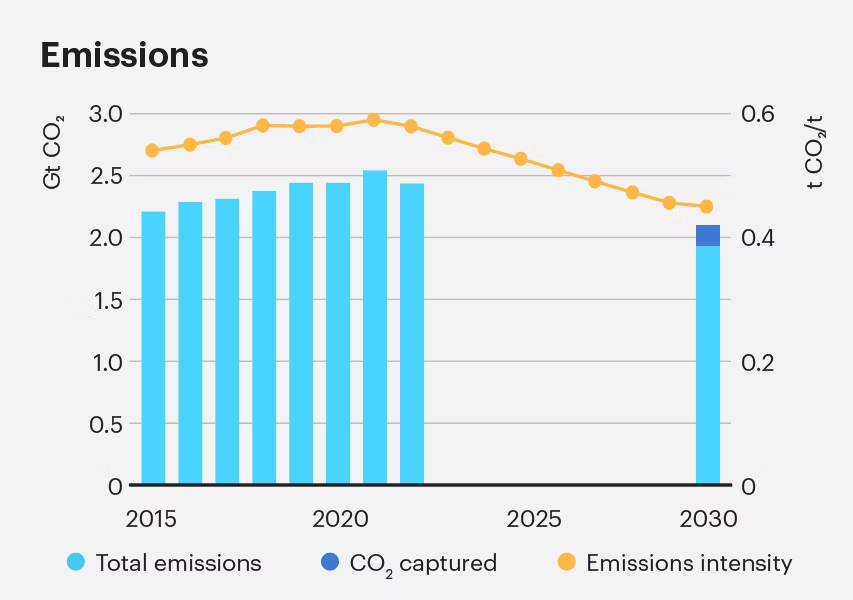

The cement sector is not on track to meet net zero by mid-century, with total emissions rising since 2015. A significant number of new high-emission cement plants are anticipated, with relatively few announcements for new near-zero emission cement projects.

- Total CO2 emissions from the cement sector have been rising since 2015.

- Emissions intensity of cement production has risen by nearly 10% since 2015, largely due to an increase in the clinker-to-cement ratio in China.

- By 2030, total emissions need to fall by around 20%, enabled in part by an increase in CCUS.

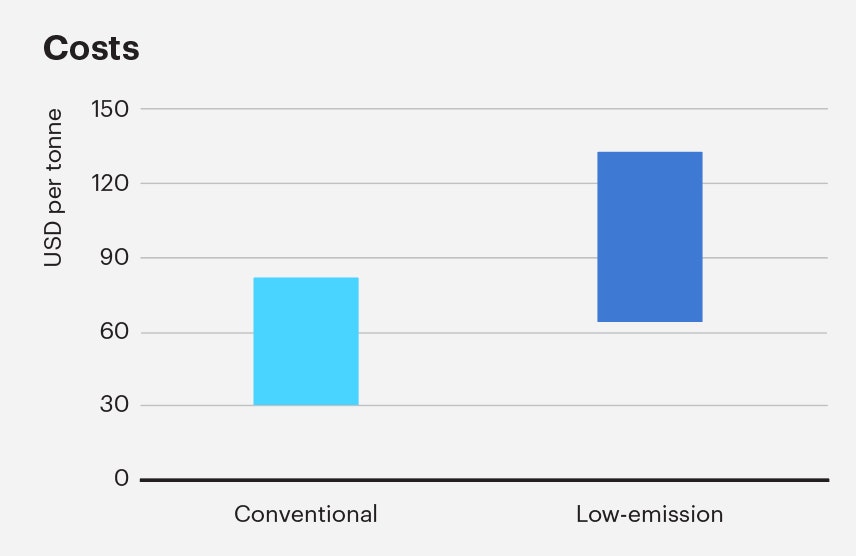

- During the 2020s, costs of producing near-zero emission cement are likely to remain significantly higher than conventional cement.

- While a range of different low-emission technologies are under development, current estimates put low-emission cement at a 75% premium versus conventional cement production, on average.

{kind=link}

{kind=link}

{kind=link}

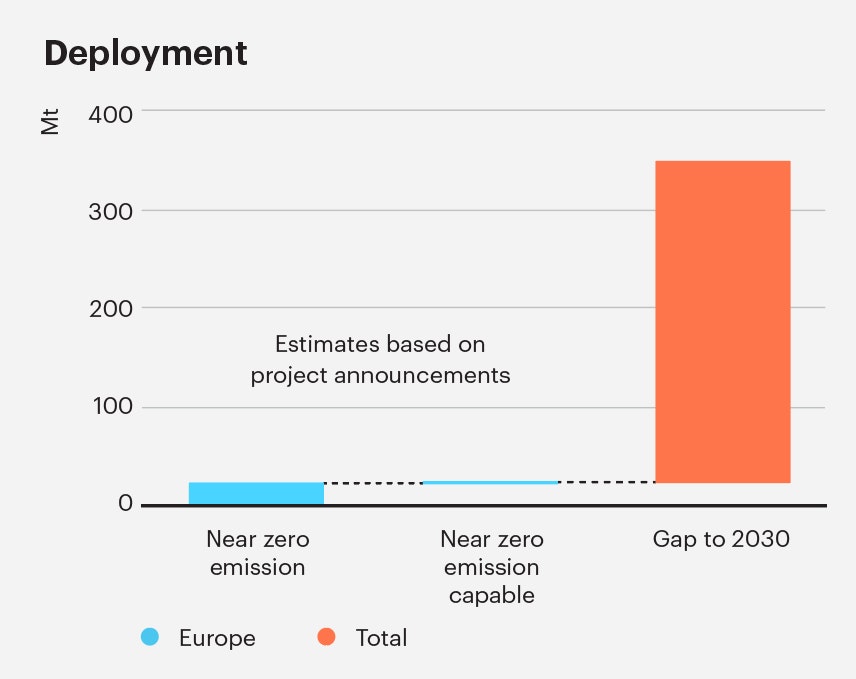

- Current announcements for near-zero emission4 cement production by 2030 are at 22 Mt, plus 2 Mt near-zero emission capable.

- The pipeline of projects has increased somewhat in recent years but remains a long way from the approximately 350 Mt required to get on track for net zero.

- By 2030, around 8% of global cement production capacity needs to be consistent with near-zero emissions.

Progress summary

| Area | What progress has been made? | What more needs to be done? | 2023 |

|---|---|---|---|

C1. Standards and certification |

Strong alignment between international organisations on production level emissions accounting. Countries and companies increasingly looking to define low and near-zero emission cement and concrete. |

Countries should agree a timeline for developing and adopting 1.5 C aligned low and near-zero emission definitions, as well as guidelines for efficient use and reuse of building material. |

|

C2. Demand creation |

Several, relatively new public and private sector forums for aggregating demand side commitments. |

Further scale-up of high-quality commitments, which should be multi-year and backed by offtake agreements and or policy support. |

|

C3. Research and innovation |

Successful private sector collaborations are well-established, focused on both pre-competitive and applied innovation. Recent launch of MI NZIM to support country-level collaboration. |

Accelerate the pace of learning among a wider set of countries, linking efforts to available financial and technical assistance. Support the delivery of pilot and demonstration scale projects for deep decarbonisation technologies. |

|

C4. Finance and investment |

Several IFIs have programmes in place which can support cement decarbonisation projects. A growing focus from countries to improve the financial and technical assistance offer for developing countries, including under the Climate Club and LeadIT. |

Develop an improved matchmaking function focused on industry decarbonisation to better respond to developing country requests and mobilise private sector investment. |

Cement recommendations

- Countries and companies should work through existing collaborative forums to agree definitions for low and near-zero emission cement and concrete by the mid-2020s, as well as guidelines for the efficient use and reuse of building material.

- Countries and companies should work through existing collaborative forums to co‑ordinate and scale up early efforts to create a market for near-zero emission cement, including via high-quality, multi-year purchase commitments and/or policy support.

- Countries should work together with effective private sector collaborative forums to accelerate the pace of learning between a wider set of countries, with a particular focus on developing countries. These partnerships should support the delivery of pilot and demonstration scale projects in all major emerging and developing countries well in advance of 2030.

- Countries should establish a matchmaking function focused on industry decarbonisation and cement that can better respond to developing country requests for financial and technical assistance. In addition to participating countries, this should include IFIs, national development banks, philanthropic organisations, private financial institutions, industry coalitions and companies, with regular meeting of ministers.